For UK small and medium-sized businesses, correctly identifying allowable business expenses is one of the most consequential tasks in financial management. HMRC business expenses rules set clear boundaries around what qualifies for tax relief, yet many SMEs, limited company directors, and self-employed professionals either under-claim through lack of awareness or over-claim through misinterpretation. Both errors carry risk.

When business expenses are misclassified, the consequences extend beyond a rejected claim. Overstated deductions may attract HMRC scrutiny or penalties. Under-claimed expenses result in a higher Corporation Tax or Income Tax liability than is legally required a direct cost to the business with a material effect on cash flow and audit readiness.

Key Takeaways:

- A structured, HMRC explained breakdown of allowable business expenses

- Clear distinction between revenue costs and capital allowances

- Differences between allowable expenses for limited company and allowable expenses for self employed

- Practical compliance and record-keeping guidance for UK SMEs

What are Allowable Business Expenses Under HMRC Rules?

Under HMRC business expenses rules, a cost qualifies as an allowable expense if it is incurred wholly and exclusively for business purposes. This principle applies to both limited companies and self-employed individuals.

Business expenses refer to day-to-day operational costs necessary to run the business. When a cost meets HMRC criteria, it becomes tax deductible, meaning it can be deducted from taxable profits before calculating tax liability.

If an expense has a dual purpose, only the business portion may be claimed. Private elements must be excluded. This distinction forms the foundation of HMRC compliance.

Complete HMRC List of Allowable Business Expenses for SMEs

The categories below reflect HMRC allowable expenses commonly claimed by UK SMEs.

Office Costs

- Rent for business premises

- Business rates and utilities

- Office supplies such as stationery

- Software subscriptions used for operations

- Telephone and broadband (business proportion only)

Travel Expenses

- Mileage for business journeys

- Train, bus and air fares for work travel

- Hotel accommodation for business trips

- Parking fees and tolls

Ordinary commuting between home and a permanent workplace is not tax deductible.

Staff Costs

- Salaries and wages

- Employer National Insurance contributions

- Pension contributions

- Bonuses and commissions

- Staff welfare facilities

Professional Fees

- Accountancy fees

- Legal fees relating to business matters

- Consultancy services

- Industry membership subscriptions

Marketing and Advertising

- Website hosting and maintenance

- Online advertising

- Printed promotional materials

- Trade directory listings

Client entertainment is generally not allowable.

Training Expenses

- Work-related training to maintain or improve existing skills

- Mandatory compliance courses

Training that introduces a new trade or qualification is usually disallowed.

Home Office Expenses

- Proportion of rent or mortgage interest

- Utilities

- Broadband

- Council tax (apportioned)

HMRC provides simplified flat rate methods or actual cost apportionment.

Insurance

- Professional indemnity insurance

- Public liability insurance

- Employers’ liability insurance

- Business vehicle insurance

Bank Charges and Interest

- Business bank account fees

- Interest on business loans or overdrafts

- Credit card processing charges

Summary of Key Allowable Expense Categories

| Category | Examples | Tax Deductible? |

|---|---|---|

| Office costs | Rent, utilities, supplies | Yes |

| Travel expenses | Business mileage, hotels | Yes (excluding commuting) |

| Staff costs | Wages, pensions | Yes |

| Marketing | Advertising, website | Yes |

| Training expenses | Skill maintenance | Yes (if relevant) |

| Insurance | Business cover | Yes |

| Bank charges | Loan interest | Yes |

Non-Allowable Business Expenses Under HMRC Rules

Not every business cost qualifies for tax relief. HM Revenue and Customs also defines non-allowable business expenses, which cannot be deducted from profits.

These usually arise when a cost is personal, capital in nature, or not incurred solely for business purposes.

Client Entertainment

Expenses related to entertaining clients are generally not tax deductible.

Examples include:

- Restaurant meals with clients

- Event or hospitality tickets

- Sporting event entertainment

Personal Expenses

Costs with a private element cannot be claimed unless the business portion is clearly separated.

Examples include:

- Personal travel

- Everyday clothing

- Household purchases

Fines and Penalties

Penalties are not considered legitimate business costs.

Examples include:

- Late filing penalties

- Parking fines

- Regulatory fines

Capital Purchases Claimed Incorrectly

Long-term assets cannot be deducted as normal expenses.

Examples include:

- Business vehicles

- Machinery and equipment

- Computers and office furniture

These fall under capital allowances instead.

Summary of Non-Allowable Expenses

| Category | Examples | Tax Deductible |

|---|---|---|

| Client entertainment | Meals, hospitality events | No |

| Personal expenses | Private travel, clothing | No |

| Fines and penalties | Parking fines, late penalties | No |

| Capital purchases | Vehicles, machinery | No (capital allowances apply) |

Allowable Expenses for Limited Company vs Self-Employed

The core rules are similar, but tax treatment differs in structure.

| Area | Allowable Expenses for Limited Company | Allowable Expenses for Self Employed |

|---|---|---|

| Tax system | Deducted before Corporation Tax | Deducted before Income Tax |

| Director salary | Treated as staff cost | Not applicable |

| Dividends | Not an expense | Not applicable |

| Personal drawings | Not allowable | Not allowable |

| Pension contributions | Employer contributions deductible | Personal pension relief rules apply |

| Capital allowances | Claimed by company | Claimed by individual |

Allowable expenses for limited company must be incurred by the company, not personally by directors unless properly reimbursed.

Allowable expenses for self-employed individuals must meet the wholly and exclusively rule and be declared within Self-Assessment.

Capital Allowances vs Revenue Expenses

A key distinction within business expenses is between revenue costs and capital allowances.

Revenue expenses are day-to-day running costs such as rent, utilities and travel expenses. These are deducted directly from profits in the accounting period incurred.

Capital allowances apply to longer-term assets such as:

- Office equipment

- Machinery

- Business vehicles

- IT hardware

Instead of deducting the full cost as a revenue expense, tax relief is given through capital allowances. The Annual Investment Allowance often permits full relief in the year of purchase, subject to limits.

For example, purchasing a laptop for daily operations falls under capital allowances rather than standard business expenses.

Understanding this distinction prevents incorrect deductions and supports accurate HMRC compliance.

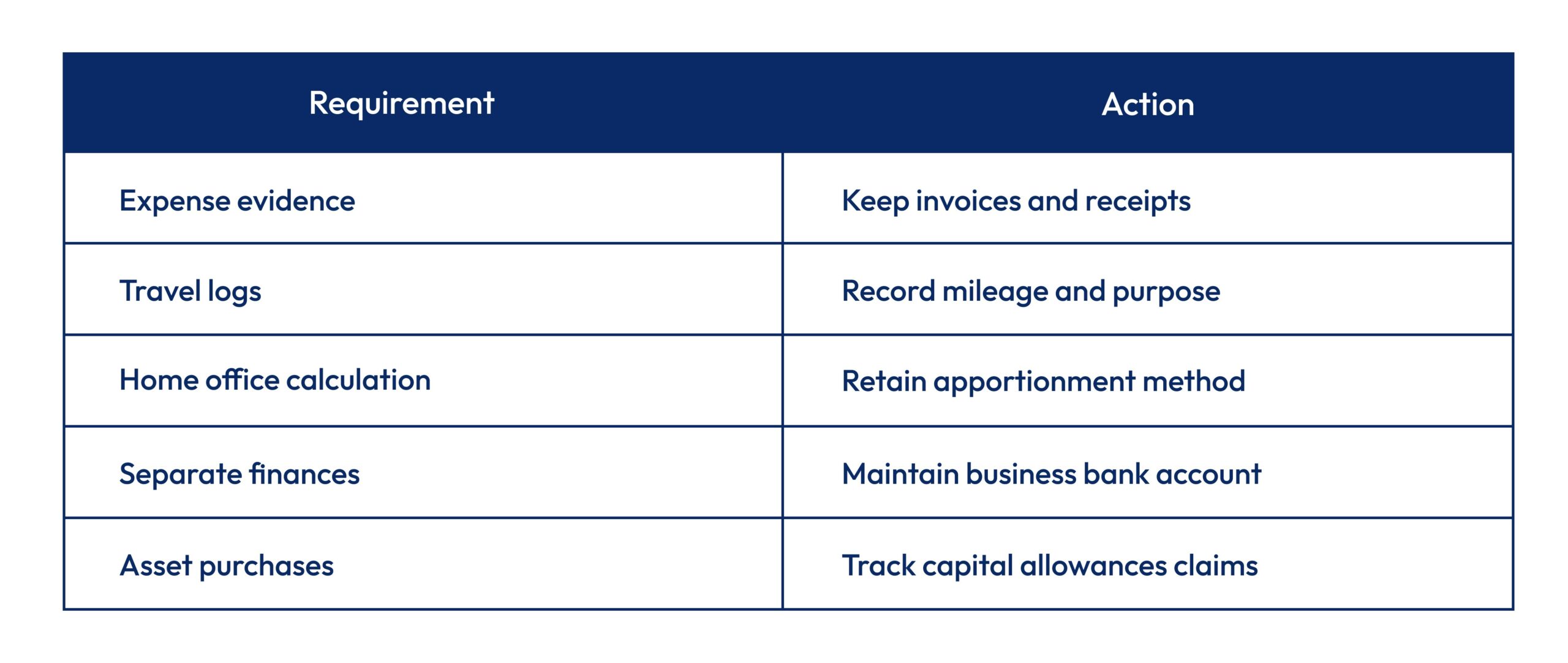

HMRC Compliance and Record Keeping

HMRC compliance requires clear evidence supporting each expense claim. HMRC explained guidance confirms that businesses must retain:

- Invoices and receipts

- Bank statements

- Mileage logs for travel expenses

- Home office calculation records

- Payroll documentation

Digital record-keeping is increasingly expected, particularly under Making Tax Digital requirements.

Compliance Checklist

Incomplete documentation increases risk during an enquiry.

Why Accurate Expense Recording Matters for SMEs?

Accurate recording of business expenses ensures maximum legitimate tax relief while reducing exposure to penalties. Proper classification supports:

- Reliable profit reporting

- Improved cash flow forecasting

- Strong audit readiness

- Reduced HMRC compliance risk

Well-maintained records also support collaboration with bookkeeping services, provide clarity for bookkeeping support teams, and strengthen oversight when using outsourcing accounting arrangements.

Consistent processes protect both tax efficiency and operational control.

Conclusion

Understanding allowable business expenses under UK tax law is essential for SMEs seeking clarity and compliance. This guide has provided a complete HMRC explained breakdown of eligible categories, distinctions between allowable expenses for limited company and allowable expenses for self-employed, and the critical difference between revenue costs and capital allowances.

By applying HMRC business expenses rules carefully, maintaining structured records, and ensuring accurate classification, businesses can secure legitimate tax relief while minimising compliance risk.

Professional bookkeeping support can help ensure expenses are recorded accurately and remain fully compliant.

Frequently Asked Questions

1. What qualifies as tax deductible business expenses in the UK?

Expenses must be wholly and exclusively for business purposes under HMRC business expenses rules.

2. Can commuting costs be claimed?

No. Ordinary commuting between home and a permanent workplace is not allowable.

3. Are home office expenses allowed?

Yes, either using simplified flat rates or actual cost apportionment.

4. Is client entertainment tax deductible?

Generally no, client entertainment is not an allowable expense.

5. Are training expenses always allowable?

Only if the training maintains or improves existing business skills.

6. What is the difference between revenue costs and capital allowances?

Revenue costs are daily operational expenses. Capital allowances apply to long-term assets.

7. Do limited companies and sole traders follow different rules?

The core principles are similar, but tax systems differ between Corporation Tax and Income Tax.

8. How long must expense records be kept?

Typically at least six years for UK tax purposes.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.