For 2026/27, UK dividend tax rates are 10.75% for basic rate taxpayers, 35.75% for higher rate taxpayers and 39.35% for additional rate taxpayers. The dividend allowance stays at £500. These rates rose by two percentage points on 6 April 2026, the first dividend tax increase since 2022.

The increase was confirmed at the Autumn Budget 2025 on 26 November 2025 and is now law. For years, dividends were one of the most tax-efficient ways for UK company directors to draw income. With higher rates and a £500 allowance, that gap has narrowed.

A director taking £30,000 in dividends at the higher rate now pays around £590 more a year than under the old 33.75% rate. Income tax thresholds are also frozen until April 2031, so more directors will be pulled into higher bands over time.

Key Takeaways

- Dividend tax rates rose by two percentage points on 6 April 2026: 10.75% basic, 35.75% higher and 39.35% additional (unchanged).

- The dividend allowance stays at £500 for 2026/27. The first £500 is taxed at 0% but still counts towards your income band.

- Dividend tax rates and the thresholds that set them are identical across the whole UK, including Scotland and Northern Ireland.

- Income tax thresholds are frozen until April 2031, so frozen bands plus rising income push more dividends into higher rates each year.

- From the 2025/26 tax return, directors of close companies must report each company’s dividends and shareholding separately, with a £60 penalty for each missing detail.

Dividend Tax Rates and Thresholds in 2026-27

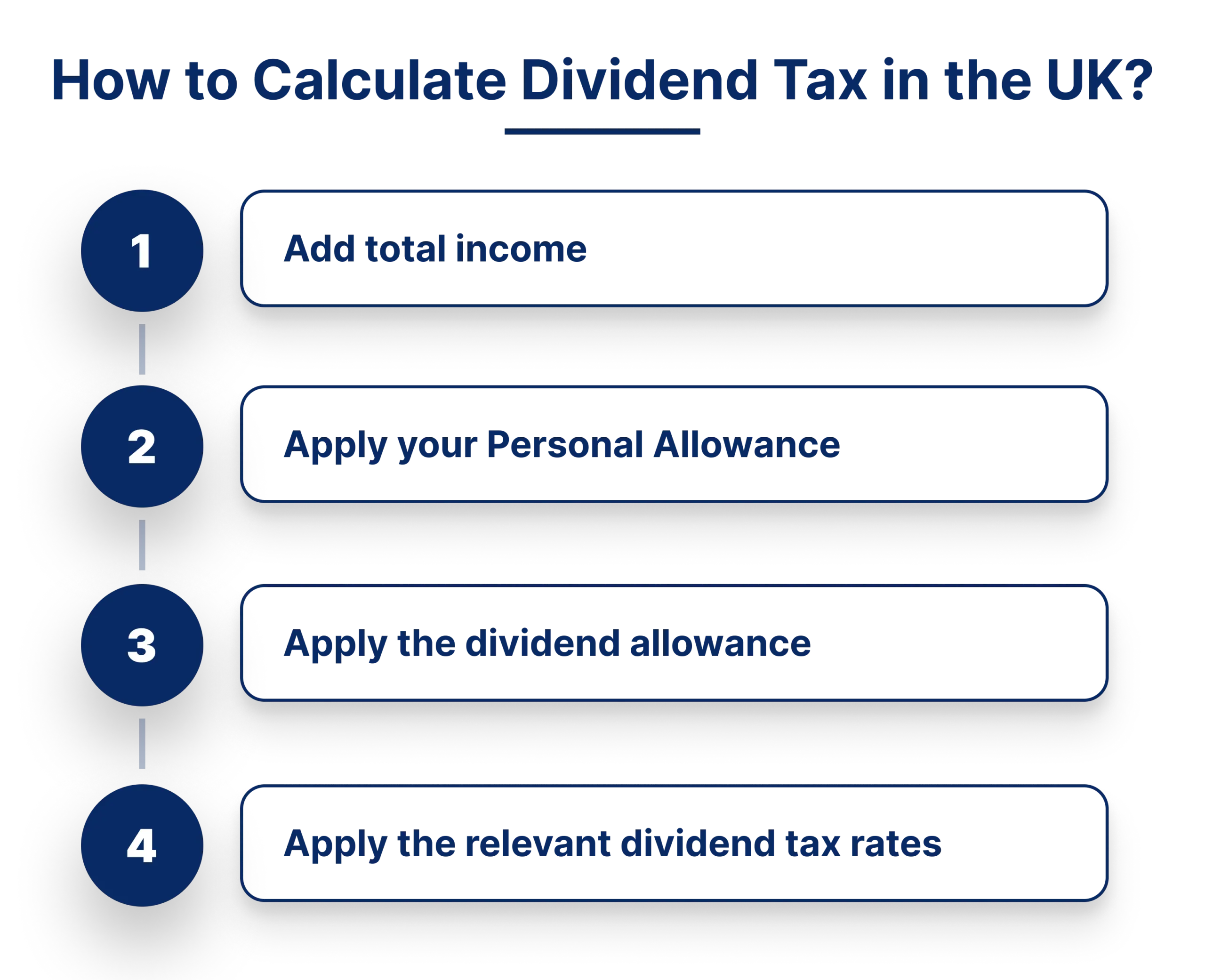

Understanding dividend tax thresholds is straightforward once you know how HMRC stacks income. Your salary is counted first, then dividends are placed on top. So a £40,000 salary with £15,000 in dividends gives a total of £55,000. That pushes those dividends into the higher rate band, not the basic rate. This is the point many directors misread on their UK tax rates on dividend income.

The HMRC dividend tax rates below apply after your Personal Allowance (£12,570) and £500 dividend allowance are used. These rates were confirmed at the Autumn Budget 2025 on 26 November 2025 and took effect from 6 April 2026.

| Total income band | Taxable band | 2025/26 rate | 2026/27 rate |

|---|---|---|---|

| Personal Allowance (up to £12,570) | 0%* | 0%* | 0%* |

| Basic rate (£12,571 to £50,270) | Basic | 8.75% | 10.75% |

| Higher rate (£50,271 to £125,140) | Higher | 33.75% | 35.75% |

| Additional rate (over £125,140) | Additional | 39.35% | 39.35% |

These figures show the dividend rate at each income band for 2025/26 and 2026/27. The first £500 of dividends, and any dividends within an unused Personal Allowance, are taxed at 0%.

Basic rate taxpayers (income £12,571 to £50,270): Dividend tax was 8.75% in 2025/26 and is 10.75% in 2026/27. For every £1,000 of dividends above the £500 allowance, you now pay £107.50, up from £87.50.

Higher rate taxpayers (income £50,271 to £125,140): Dividend tax was 33.75% in 2025/26 and is 35.75% in 2026/27. For every £1,000 of dividends above the allowance, you now pay £357.50, up from £337.50.

Additional rate taxpayers (income over £125,140): Dividend tax stays at 39.35% for both years. For every £1,000 of dividends above the allowance, you pay £393.50.

Dividend Tax in Scotland and Northern Ireland

Dividend tax rates and thresholds are the same across the whole UK. Scotland sets its own rates and bands only for earned and other non-savings, non-dividend income. Dividends are taxed using UK-wide rates and the UK rate bands.

This means a Scottish taxpayer still moves into the higher dividend rate at £50,270 of total income, the same as a taxpayer in England, Wales or Northern Ireland. The Scottish higher-rate threshold for salary does not apply to dividends.

What the 2026/27 Rates Cost You

The table below shows the tax due if all your dividends fall within a single band, before applying the £500 allowance.

| Dividend income | Basic rate (10.75%) | Higher rate (35.75%) | Additional rate (39.35%) |

|---|---|---|---|

| £10,000 | £1,075 | £3,575 | £3,935 |

| £20,000 | £2,150 | £7,150 | £7,870 |

| £30,000 | £3,225 | £10,725 | £11,805 |

| £50,000 | £5,375 | £17,875 | £19,675 |

Key insight: The additional rate of 39.35% is unchanged. Basic and higher rate taxpayers carry the full impact of the April 2026 increase. Income tax thresholds stay frozen until April 2031, so rising income will gradually push more directors into higher bands.

What is the Dividend Allowance?

The UK dividend allowance is the amount of dividend income you can receive tax-free each year before dividend tax applies.

Dividend Allowance in 2026-27

For 2026/27, the dividend allowance is £500 per tax year.

This is also called the dividend tax free allowance. It does not mean dividends are tax free. It means the first £500 is taxed at 0% but still counts towards your income band.

The allowance applies in addition to your Personal Allowance. It does not reduce your total taxable income for band purposes.

The dividend allowance has been cut sharply over the years, from £2,000 to £1,000 and now £500. With such a small tax-free threshold, most directors drawing regular dividends will have a meaningful tax liability to plan for.

Which Dividends are Taxable?

A common question is which dividends are taxable in the UK. Dividends are taxable if they are paid from:

- UK limited companies

- Overseas companies

- Unit trusts or investment funds

Dividend income taxability depends on the source and your residency status. Most UK resident directors receiving payments from their own company must report this income through Self Assessment.

Example A, basic rate: Salary £12,570 and dividends £30,000, total income £42,570. The £500 allowance is taxed at 0%. The remaining £29,500 is taxed at 10.75%, giving £3,171.25.

Example B, higher rate: Other income £55,000 and dividends £10,000. The salary already uses the higher rate band, so all dividends fall in the higher rate. The £500 allowance is taxed at 0%. The remaining £9,500 is taxed at 35.75%, giving £3,396.25.

Example C, additional rate: Other income £130,000 and dividends £10,000. All dividends fall above £125,140. The £500 allowance is taxed at 0%. The remaining £9,500 is taxed at 39.35%, giving £3,738.25.

Where total income crosses a threshold, dividends are split across bands. For example, salary £12,570 and dividends £45,000 gives total income of £57,570. After the £500 allowance, £37,200 of dividends is taxed at 10.75% (£3,999) and £7,300 at 35.75% (£2,609.75), for a total of £6,608.75.

Most Tax-Efficient Salary and Dividend Combination for 2026/27

For most limited company directors, the most tax-efficient approach is to pay a salary up to a National Insurance threshold and take the remainder as dividends. Here is how the numbers work for 2026/27.

| Salary | Dividends | Total income | Estimated personal tax | Why this combination |

|---|---|---|---|---|

| £12,570 | £0 | £12,570 | £0 | Salary within Personal Allowance, so no income tax and no employee NI. |

| £12,570 | £37,200 | £49,770 | ~£3,945 | Maximises the basic rate band. Dividends taxed at 10.75% after the £500 allowance. |

| £12,570 | £50,000 | £62,570 | ~£8,396 | Dividends above £50,270 enter the higher rate of 35.75%. Pension contributions worth reviewing. |

The figures above show dividend tax only. They do not include any employer National Insurance on the salary.

The standard approach for 2026/27 is to pay a salary that uses your Personal Allowance, then take remaining profits as dividends up to the basic rate band limit of £50,270. Two points decide the right salary level:

- Employer National Insurance. The secondary threshold is £5,000 for 2026/27, with employer NI charged at 15% above it. A salary above £5,000 creates an employer NI cost unless it is covered by the Employment Allowance.

- Employment Allowance. Companies with at least one other employee can use the £10,500 Employment Allowance to cover the employer NI on a £12,570 salary. Sole-director companies with no other employees cannot claim it, so they weigh the employer NI against the Corporation Tax saving on the higher salary.

To earn a qualifying year towards the State Pension, you need earnings at or above the Lower Earnings Limit, which is £6,708 for 2026/27. A salary set only at the £5,000 secondary threshold sits below this, so it would not count.

Keeping dividends within the basic rate band holds your dividend tax at 10.75% and avoids the 35.75% higher rate. A spouse or civil partner in a lower income band can also receive dividends from shares in your company, which reduces your combined household tax.

Warning: The £100,000 Personal Allowance Trap

If your total income from salary and dividends exceeds £100,000, your Personal Allowance starts to taper. It reduces by £1 for every £2 of income above this threshold. By £125,140, your Personal Allowance is fully withdrawn.

This withdrawal adds a hidden layer of tax, creating an effective marginal rate of up to around 60% on income in this band. For directors approaching it, the priority actions are:

- Make pension contributions to reduce adjusted net income below £100,000.

- Defer dividend declarations to the next tax year where possible.

- Review Gift Aid donations, which also reduce adjusted net income.

Reviewing your position before 5 April matters most if your combined income is approaching this threshold.

Limited Company Tax on Dividends vs Corporate Tax

There is often confusion between corporate tax on dividends and personal dividend tax.

A limited company pays Corporation Tax on its profits first. Only after that can dividends be issued. For example, a company with £100,000 of profit pays Corporation Tax, and only the remaining profit can be distributed. The director then pays personal tax under the limited company tax on dividends rules.

Dividends are not a deductible business expense. They are distributions of post-tax profit.

How to Pay Dividend Tax?

Once your dividend income produces a tax liability, reporting to HMRC is a legal requirement. Self Assessment is the standard method. File and pay by 31 January 2028 for the 2026/27 tax year.

If your dividends are modest, HMRC can adjust your tax code to collect the liability automatically from salary or pension through PAYE.

For tax purposes, the declaration date, not the payment date, sets which tax year a dividend falls into. If you are planning dividends around the year end, the date the board formally approves them is what counts.

New Reporting Rules for Company Directors

From the 2025/26 tax return, directors of close companies must give HMRC more detail about their dividends. The first returns affected are due by 31 January 2027.

You must report the name and registration number of each company you received dividends from, the dividend amount from each close company separately, even if it is zero, and your highest shareholding percentage during the year. HMRC can charge a £60 penalty for each missing or incorrect detail, separate from any late-filing penalty.

The method for calculating dividend tax has not changed. These rules are about reporting, not new rates.

Late filing brings an automatic £100 penalty. Late payment attracts interest from the deadline, plus 5% surcharges at 30 days, 6 months and 12 months.

How to Reduce Your Dividend Tax Bill in 2026?

With rates higher than last year and thresholds frozen, more directors are paying more tax without changing anything. There are legitimate, HMRC-approved ways to reduce what you owe, and most are straightforward.

- Stocks and Shares ISA: Dividends inside an ISA are fully exempt, with a £20,000 annual allowance. At the higher rate, sheltering £20,000 of dividends in an ISA saves up to £7,150 a year.

- Pension contributions: These reduce your taxable income and can drop you into a lower band, up to a £60,000 annual allowance. A higher rate taxpayer contributing £10,000 saves around £3,575 in dividend tax, and the contribution itself attracts tax relief at your marginal rate.

- Spousal transfers: Transferring dividend-paying shares to a spouse in a lower band reduces your combined liability. If your spouse pays basic rate tax on £10,000 of dividends, their tax is £1,075 against £3,575 at your higher rate, a saving of £2,500 on that income.

- Timing dividend declarations: The declaration date sets the tax year. Reviewing your position before 5 April can keep you in a lower band.

Common Dividend Tax Mistakes

Even directors with experienced accountants get caught out by the same handful of issues each year. The mistakes below are the ones that most often lead to unexpected tax bills, HMRC enquiries or missed planning opportunities.

Forgetting that the £500 allowance still counts towards your band. The first £500 of dividends is taxed at 0%, but it still occupies space in your basic, higher or additional rate band. Readers often treat the allowance as if it sits outside the tax bands entirely. It does not.

Assuming all dividends sit in one band. If your total income straddles a threshold, dividends are split across bands and taxed at different rates on each slice. A director with a £12,570 salary and £45,000 in dividends does not pay 10.75% on the lot. Around £37,200 falls in the basic rate and £7,300 falls in the higher rate. Calculating at a single rate understates the bill.

Using the payment date instead of the declaration date. For tax purposes, a dividend falls in the tax year it is declared, not the year it is paid. A board resolution dated 5 April 2026 falls in 2025/26. The same resolution dated 6 April 2026 falls in 2026/27 at the new rates. Directors planning year-end dividends should confirm the date the board formally approves them.

Missing the new close company reporting rules. From the 2025/26 tax return onwards, directors of close companies must list each company’s dividends, registration number and highest shareholding percentage separately. HMRC can charge £60 per missing or incorrect detail, on top of any late-filing penalty. Many directors are not yet aware this is in force.

Ignoring the £100,000 Personal Allowance taper. Once total income exceeds £100,000, the Personal Allowance reduces by £1 for every £2 of income above that level. Pushing dividends into this band creates an effective marginal rate of around 60%, not 35.75%. Pension contributions or deferring dividends can avoid this trap, but only if the position is reviewed before 5 April.

Treating dividends as a deductible business expense. Dividends are distributions of post-tax profit, not an expense for the company. They do not reduce the company’s Corporation Tax bill. Recording them as expenses in the accounts is a common bookkeeping error that creates problems at year end.

Not using a Stocks and Shares ISA where available. Dividends inside an ISA are fully exempt from dividend tax. For directors holding investment portfolios outside an ISA, this is often the simplest reduction strategy and the one most frequently overlooked.

Dividend Tax Planning Considerations

Directors should review dividend tax thresholds before year end, income splitting between spouses where appropriate, the timing of dividend declarations, and the interaction with Child Benefit and Personal Allowance tapering. This supports efficient management of dividend income without breaching compliance rules.

Conclusion

This guide explains Dividend Tax in the UK for 2026/27, including current dividend tax rates, the £500 dividend allowance and a clear method to calculate tax on dividends in the UK.

Understanding dividend tax thresholds, which dividends are taxable and how to pay dividend tax helps directors avoid unexpected liabilities and stay compliant. With the allowance limited to £500 and rates two percentage points higher since April 2026, effective planning is essential for UK limited company owners. Frozen thresholds until 2031 mean more income will fall into higher bands over time, so proactive planning matters more each year.

For most directors, the most tax-efficient approach in 2026/27 remains a salary that uses the Personal Allowance combined with dividends within the basic rate band.

Use our free Dividend Tax Calculator to model your position and make informed decisions. Speak to our dividend tax specialists today at info@outbooks.co.uk or call on +44 330 057 8597.

FAQs

What is the dividend allowance for 2026/27?

The dividend allowance for 2026/27 is £500. This amount is taxed at 0% but still counts towards your total taxable income band.

What are the dividend tax rates for 2026/27?

HMRC dividend tax rates for 2026/27 are 10.75% for basic rate, 35.75% for higher rate and 39.35% for additional rate taxpayers.

How much tax will I pay on £30,000 in dividends?

With a £12,570 salary, £30,000 in dividends gives a basic rate bill of about £3,171, after the £500 allowance, at the 10.75% rate.

How do I calculate tax on dividends in the UK?

Add dividends to your total income, apply your Personal Allowance and the £500 dividend allowance, then apply the correct UK dividend tax rate to each band.

Does a limited company pay tax on dividends?

The company pays Corporation Tax on profits first. Directors then pay personal tax on the dividends they receive under the limited company tax on dividends rules.

How do I report and pay dividend tax?

You report dividends through Self Assessment and pay by 31 January after the tax year. Directors of close companies must now report each company’s dividends separately.

What happens to my Personal Allowance above £100,000?

It reduces by £1 for every £2 above £100,000 and is fully withdrawn at £125,140. This creates an effective marginal rate of up to around 60%.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.