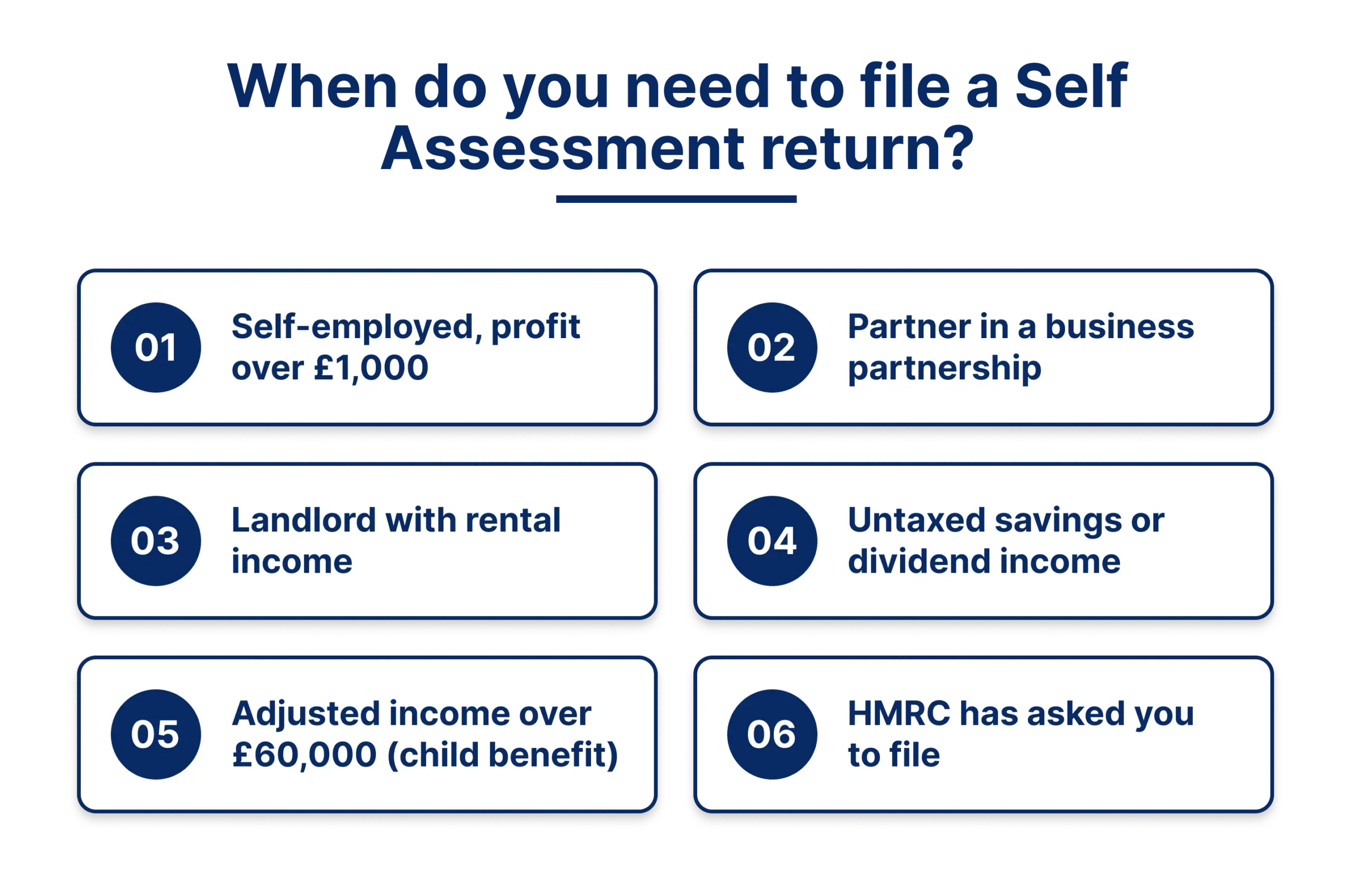

Self Assessment for landlords is the process of reporting rental income, allowable expenses and taxable property profits to HMRC. If your total rental income exceeds the £1,000 property income allowance in a tax year, you may need to complete a Self Assessment tax return and pay tax on your rental profits.

From 6 April 2026, landlords with qualifying income over £50,000 must also report under Making Tax Digital (MTD) for Income Tax. That means quarterly digital updates instead of a single annual return.

Key Takeaways

- Landlords earning over £1,000 in rental income may need to file a Self Assessment tax return.

- Allowable expenses such as repairs, insurance and agent fees reduce taxable rental profits.

- Mortgage interest is not an allowable expense. Residential landlords get a 20% basic-rate tax credit instead.

- Online tax returns for the 2025/26 tax year must be submitted by 31 January 2027.

- From 6 April 2026, landlords with qualifying income over £50,000 must follow MTD for Income Tax and keep digital records.

Do Landlords Need to Do a Tax Return?

Not every landlord needs to file a return. The requirement depends on your rental income.

If your total annual gross property income is £1,000 or below, there is usually no need to tell HMRC. This is the property income allowance.

You must file a Self Assessment return if you earn above this threshold. Each joint owner declares their own share of rental income and expenses separately on their individual return.

When filing becomes mandatory

You need to file a Self Assessment return in several situations. These include earning more than £1,000 from UK rental property, having taxable rental profits, or wanting to claim expenses or losses.

Overseas property income also needs reporting on your return. Note that the Furnished Holiday Lettings regime was abolished from 6 April 2025. Holiday lets are now taxed as ordinary property income, with no separate reporting or reliefs.

From 6 April 2026, landlords with qualifying income over £50,000 must also comply with MTD for Income Tax. Qualifying income is your gross income from self-employment and property combined, before expenses. You are in scope if that total tops £50,000, even if it comes from property alone.

How to Declare Rental Income in the UK

Declaring rental income starts with registering for Self Assessment online. You need to register by 5 October following the tax year you had profits in. HMRC then sends you a Unique Taxpayer Reference (UTR) number.

This UTR is essential for all future returns, so keep it safe.

Registration process

First, register online through the HMRC website. You will need personal details including your National Insurance number.

For the 2025/26 tax year, you must register by 5 October 2026. HMRC sends your UTR by post, usually within 10 working days.

Typical landlord Self Assessment workflow

In practice, many landlords follow a structured workflow across the year:

- Monthly rental income tracking through bank feeds or spreadsheets

- Categorising expenses as they occur, such as repairs, agent fees and insurance

- A quarterly profitability review to estimate tax exposure

- Year-end reconciliation before completing the SA105 property pages

This workflow helps landlords avoid year-end surprises and supports accurate reporting. Digital accounting tools can simplify it and improve accuracy.

Also read: HMRC Targets Personal Expense Claims, Key Tax Updates for Sole Traders and Landlords

How to File a Self Assessment as a Landlord

Filing involves the SA100 main return plus the SA105 supplementary pages for property income.

Log into your HMRC online account using your UTR. Go to the Self Assessment section and start your return. Complete each section with your rental figures and include all allowable expenses to reduce taxable profit.

For landlords with several properties, structured bookkeeping improves accuracy and makes reporting faster.

Declaring Rental Income: Step-by-Step

Start by gathering your rental income records. Calculate gross rental income for the tax year, covering all rent received from 6 April to 5 April.

Add any extra charges from tenants, such as service charges or utility payments you collect. Accurate figures here are essential.

Income calculation methods

You report on either the cash basis or the accruals basis. Cash basis records income when money arrives in your account. Accruals basis records income when it is earned, not received.

The cash basis is now the default for most individual landlords. It is simpler and matches your actual cash flow. You can elect to use the accruals basis instead, which can suit larger or more complex portfolios.

Self Assessment Tax Return for Rental Property: Worked Examples

Here is a simple example. You receive £12,000 in annual rent and pay £2,000 in allowable expenses such as repairs and agent fees. Your taxable profit is £10,000.

This £10,000 is added to your other income and taxed at your marginal rate.

Example with a mortgage

Now add a £4,000 mortgage interest cost. Mortgage interest is not deducted as an expense, so your taxable profit stays at £10,000 (£12,000 minus £2,000).

Instead, you claim a basic-rate tax reducer worth 20% of the £4,000 interest, which is £800.

- A higher-rate (40%) landlord pays £4,000 tax on the £10,000 profit, then deducts the £800 credit. Tax due is £3,200.

- A basic-rate (20%) landlord pays £2,000, then deducts £800. Tax due is £1,200.

This shows why the change hits higher-rate landlords hardest. They no longer get full relief on mortgage interest.

Can You Deduct Mortgage Interest on a Rental Property?

No. Since 6 April 2020, residential landlords cannot deduct mortgage interest or other finance costs from rental income. This is the Section 24 finance cost restriction.

Instead, you get a tax reduction worth 20% of your finance costs. Finance costs include mortgage interest, interest on loans to buy furnishings, and fees for taking out or repaying a mortgage. Capital repayments never qualify.

The credit is the lower of your finance costs, your property profits, or your adjusted total income above the personal allowance, multiplied by 20%. Any unused amount carries forward to future years.

Rental Income Self Assessment Deadlines

There are key dates every landlord must remember.

For the 2025/26 tax year, register by 5 October 2026. Paper returns are due by 31 October 2026. Online returns and payment are due by 31 January 2027. Online filing gives you an extra three months over paper.

Payment deadlines

You must pay any tax owed by 31 January, the same date as your online return.

If your bill is over £1,000, you may also make payments on account toward the next year. The first is due by 31 January and the second by 31 July. Missing a payment leads to interest from the due date until you pay.

Landlord Allowable Expenses for Self Assessment

Allowable expenses are the day-to-day running costs of the property. Only genuine business costs qualify for tax relief. Keep all receipts and invoices, as HMRC may ask for proof.

What expenses can landlords claim?

Many costs qualify. Property repairs and maintenance, buildings and contents insurance, letting agent and management fees, legal fees for tenant issues, and accountancy fees for your return are all allowable. Ground rent, service charges and any utility bills you pay also qualify.

This table lists the most common allowable expenses landlords claim.

| Expense type | Examples | Notes |

|---|---|---|

| Property maintenance | Repairs, painting, plumbing | Day-to-day repairs and maintenance only |

| Insurance | Buildings, contents, landlord insurance | Property-related policies |

| Professional fees | Letting agent, accountant, legal fees | Must relate to the rental business |

| Utilities | Water, gas, electricity | Only if paid by the landlord |

| Council Tax | Council Tax charges | Usually when the property is vacant |

| Cleaning and gardening | Cleaning, gardening, waste removal | Between tenancies or ongoing |

| Replacement of domestic items | Sofas, beds, white goods | Like-for-like replacements, not initial purchase |

| Travel costs | Property inspections and visits | Must relate wholly to rental activity |

Note: Mortgage interest is not in this table. It is claimed as a 20% tax credit, not an allowable expense. See the section above.

Also read: Accounting Pricing Strategies for Diverse Business Structures

Non-allowable expenses

Not all costs can be claimed. Capital improvements that add value cannot be deducted. Personal costs unrelated to the rental business do not qualify. The capital part of mortgage repayments is not allowable, and neither is the value of your own time or labour.

Costs incurred before you started letting the property generally cannot be claimed either.

How to Legally Reduce Tax on Rental Income

You can lower your rental tax bill within the rules. Claim every allowable expense rather than the £1,000 allowance if your costs are higher. Claim the 20% finance cost credit on mortgage interest. Split income correctly between joint owners so each uses their personal allowance and bands.

Keeping clean records all year means you do not miss deductible costs at filing time.

Tax Rates on Rental Profit

Rental profits are added to your other taxable income and taxed at your income tax band.

| Income band | Tax rate | Annual income range |

|---|---|---|

| Personal allowance | 0% | Up to £12,570 |

| Basic rate | 20% | £12,571 to £50,270 |

| Higher rate | 40% | £50,271 to £125,140 |

| Additional rate | 45% | Over £125,140 |

Because rental income stacks on top of other earnings, it can push you into a higher band.

Late Filing Penalties for Landlord Self Assessment

HMRC issues automatic penalties for late returns. These standard Self Assessment penalties apply to landlords filing an annual return.

- £100 fixed penalty if your return is up to three months late, even if you owe no tax.

- Daily penalties of £10 after three months, up to £900.

- A further £300 or 5% of tax due at six months, and again at twelve months.

If you fail to tell HMRC you have rental profits by the 5 October deadline, you may also face a ‘failure to notify’ penalty, based on the tax owed and how late you are.

Landlords inside MTD for Income Tax face a separate points-based system. As confirmed by HMRC, there are no penalties for late quarterly updates during the 2026/27 tax year.

Selling a rental property

If you sell a residential property at a gain, you must report it and pay the estimated Capital Gains Tax within 60 days of completion, using HMRC’s online Capital Gains Tax on UK Property service. Missing this leads to an automatic £100 penalty.

Property Income Allowance vs Claiming Expenses

You can use the £1,000 property income allowance or claim actual expenses, but not both. The allowance is automatic and needs no records.

For most landlords, claiming actual expenses gives a lower tax bill. The allowance suits landlords with very low costs or income.

| Scenario | Best option |

|---|---|

| Low expenses (under £1,000) | Property income allowance |

| High repairs or management costs | Claim actual expenses |

| Simple single property | Allowance may be enough |

| Portfolio landlords | Expense method is usually better |

You can switch method each year. Work out your total allowable expenses first, then choose whichever leaves you paying less.

Record Keeping for Landlords

Good records are essential for accurate returns. Keep all financial records for at least five years after the 31 January submission deadline.

Save rental agreements, tenant correspondence and receipts for every expense you claim. Bank statements showing rent received are strong evidence. Digital tools simplify this and are now required for landlords in MTD.

Making Tax Digital: Mandatory from 6 April 2026

From 6 April 2026, MTD for Income Tax is mandatory for landlords whose qualifying income from property and self-employment exceeds £50,000. Those in scope must keep digital records using HMRC-recognised software.

You submit four quarterly updates, due 7 August, 7 November, 7 February and 7 May, followed by a Final Declaration by 31 January. The previously proposed End of Period Statement has been scrapped, so only the quarterly updates and Final Declaration are required.

The threshold drops to £30,000 from April 2027 and £20,000 from April 2028, so most landlords will be brought in over time. You can check your start date and the rules through the GOV.UK MTD step-by-step guide.

Essential documents checklist

- Monthly rent records from all tenants

- Receipts for repairs, maintenance and improvements

- Insurance documents and premium payments

- Letting agent statements and invoices

- Utility bills you pay as landlord

- Professional fees invoices (accountant, solicitor, agent)

- Mortgage statements showing interest charged

- Mileage logs for property-related travel

- Tenancy agreements and lease documents

Digital vs paper records

With MTD live, in-scope landlords must use HMRC-recognised software. If you work with an accountant, they will choose compatible software or bridging tools that connect existing spreadsheets to HMRC.

Digital records protect against loss, categorise income and expenses automatically, and connect to your bank for faster transaction recording. Make sure backups are secure and accessible.

Common Mistakes to Avoid

Many landlords make preventable errors. Missing the registration deadline is a frequent and costly one. Others forget to include all rental income, claim non-allowable expenses, or mix personal costs with business costs.

Why rental income errors trigger HMRC enquiries

- Cause: Incomplete income reporting, mixed personal expenses, missing records

- Impact: Penalties, enquiry notices, delayed tax clearance

- Solution: Keep transaction-level records, reconcile annually, and retain evidence for at least five years

When landlords seek professional support

- Managing multiple properties or mixed income sources

- Unsure whether a cost is allowable or capital

- Repeated filing errors or HMRC queries

- Preparing for MTD reporting

- Wanting tax planning beyond basic compliance

Professional support improves accuracy, lowers risk and frees time for managing the properties.

Landlord Self Assessment Checklist

- Register by 5 October

- Keep income and expense records all year

- Choose the allowance or the expenses method

- Complete the SA100 and SA105 forms

- Submit by 31 January

- Pay tax owed on time

Conclusion

Managing landlord Self Assessment correctly keeps you compliant with HMRC and helps you avoid penalties. Accurate records, correct income reporting and claiming every allowable expense reduce your tax bill and improve financial visibility.

MTD for Income Tax is live for landlords with qualifying income over £50,000, with the threshold dropping to £30,000 in April 2027 and £20,000 in April 2028. If you have not moved to HMRC-recognised software and set up quarterly reporting, now is the time.

Whether you own one property or a larger portfolio, preparing your return early and understanding your MTD obligations will keep you compliant through the year. To get help with rental accounts, quarterly MTD submissions or your Self Assessment return, contact the Outbooks team on [phone] or [email].

Frequently Asked Questions

When do I need to register for Self Assessment as a landlord?

Register by 5 October following the tax year you first earned rental income above the £1,000 allowance.

Can I claim mortgage interest on a rental property?

Not as an expense. Residential landlords get a 20% basic-rate tax credit on mortgage interest instead, under the Section 24 finance cost rules.

What happens if I miss the 31 January deadline?

For an annual Self Assessment return, you get an automatic £100 penalty. Landlords inside MTD face a separate points-based system instead.

Do I need to report rental income from Airbnb?

Yes. Airbnb and other short-let income must be declared. Since April 2025 it is taxed as ordinary property income.

Can I change from the property income allowance to expenses each year?

Yes. You can choose whichever is more beneficial each year, as long as you keep accurate records.

Do joint landlords need separate Self Assessment returns?

Yes. Each owner reports their share individually, based on their ownership percentage.

Do I need software for my tax return now?

From 6 April 2026, landlords with qualifying income over £50,000 must use HMRC-recognised software and submit quarterly updates. Below that, software is recommended but optional.

What are the MTD quarterly deadlines?

The four quarterly updates are due 7 August, 7 November, 7 February and 7 May, followed by a Final Declaration by 31 January.

How Do Landlords Calculate Taxable Rental Profit?

Taxable rental profit equals gross rental income minus allowable expenses, or minus the £1,000 allowance if you choose it. Mortgage interest is excluded, then claimed back as a 20% tax credit. The profit is added to your other income and taxed at your marginal rate.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.