HMRC has started sending digital warning emails and prompts to taxpayers in 2025, targeting personal expenses incorrectly claimed as business expenses.

If you are a sole trader, landlord, or self-employed, this does not automatically mean an investigation but it does mean HMRC is checking your expense claims more closely than before.

The focus is on mixed personal and business expenses, especially where claims exceed £2,500 per year. HMRC’s automated systems now flag these claims during Self-Assessment submission.

This guide explains why HMRC is contacting taxpayers, what expense categories are under scrutiny, and what you should fix now to avoid penalties.

What Has Changed in HMRC Expense Monitoring (2026 Update)

HMRC’s personal expense monitoring programme, introduced during the 2025 Self-Assessment cycle, continues into 2026 with broader digital prompts, stronger analytics, and behavioural nudges across filing journeys. Key developments include:

- Expansion of digital prompts during Self-Assessment completion

- Comparative analytics across similar industries and taxpayer profiles

- Integration with Making Tax Digital record-keeping expectations

- Greater use of behavioural messaging instead of immediate enquiries

Quick Takeaways:

- HMRC is actively checking personal vs business expenses

- Automated systems flag claims over £2,500

- Emails and digital warnings are part of the campaign

- Sole traders and landlords face higher scrutiny

- Correct apportionment and records reduce penalties

I Received an HMRC Expenses Email – Should I Be Worried?

Most HMRC expenses emails in 2025 are educational warnings, not formal investigations. HMRC uses these messages to remind taxpayers about the wholly and exclusively rule before returns are submitted.

However, you should take the email seriously if:

- Your expenses exceed £2,500

- You claim home office, vehicle, or travel costs

- You mix personal and business use

If errors exist, correcting them before submission or via voluntary disclosure significantly reduces penalties.

What Is HMRC’s Personal Expense Claims Campaign?

HMRC’s 2025–2026 digital campaign uses automated prompts, emails, and online warnings to prevent taxpayers from claiming personal expenditure as business expenses.

Many taxpayers see this as:

- An HMRC expenses email

- A digital advert or message during Self-Assessment

- A warning asking if expenses exceed £2,500 in a tax year

The campaign applies to 2024/25 and 2025/26 Self-Assessment returns and forms part of HMRC’s wider compliance and Making Tax Digital strategy.

HMRC personal expense campaign (definition)

HMRC’s personal expense campaign is a digital compliance initiative using automated prompts, analytics, and behavioural messaging to reduce incorrect mixed-use expense claims within Self-Assessment submissions.

HMRC Digital Campaign 2025–2026

HMRC has shared a document with ICAEW which explains that the digital campaign follows a trial in 2024. The trial results prompted this expanded enforcement programme. Self-Assessment tax return 2025 HMRC submissions face increased automated checks.

HMRC’s 2025 expense compliance checks uses advanced analytics software. The system identifies patterns suggesting inappropriate expense claims. Artificial intelligence algorithms compare similar business profiles automatically. Source: ICAEW, Aug 2025

Digital validation occurs during the submission process now. Previously flagged issues trigger immediate warnings or enquiries. This proactive approach prevents incorrect claims reaching completion.

This initiative aligns with broader UK compliance developments including Making Tax Digital for Income Tax, HMRC behavioural insights programmes, and increasing reliance on digital bookkeeping platforms such as Xero, QuickBooks, and FreeAgent for evidence readiness.

HMRC Personal expenses & Business Expenses Tax UK – Target Reason

HMRC discovered significant problems with “disallowable private use in business expenditure” during their initial trial. The substantial revenue generated from correcting these errors has prompted this focused approach. The HMRC expense review process initiative represents their most comprehensive compliance effort yet.

HMRC will now open more enquiries specifically targeting taxpayers who claim personal expenses as business deductions. This initiative follows successful identification of widespread non-compliance in expense apportionment.

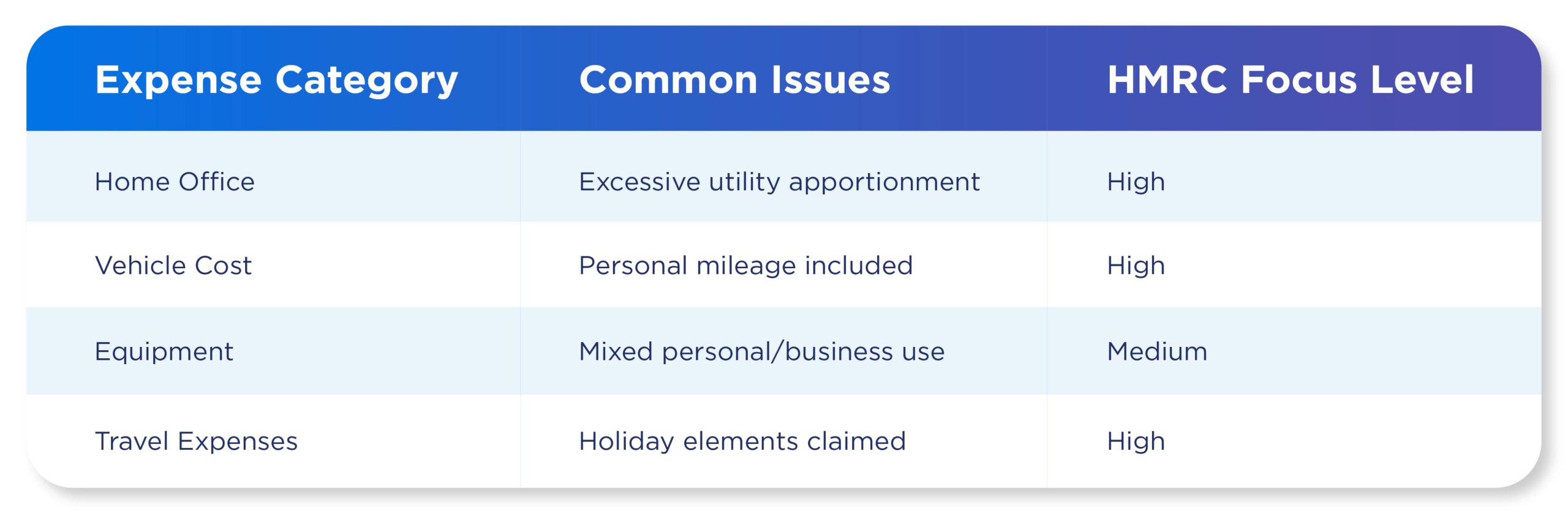

| Expense Category | Common Issues | HMRC Focus Level |

|---|---|---|

| Home Office | Excessive utility apportionment | High |

| Vehicle Costs | Personal mileage included | High |

| Equipment | Mixed personal/business use | Medium |

| Travel Expenses | Holiday elements claimed | High |

Understanding the Wholly & Exclusively Rule

The fundamental principle governing business expense claims requires expenses to be incurred “wholly and exclusively for trade purposes.” This rule forms the cornerstone of legitimate business expense claims. Understanding this principle is important for avoiding HMRC penalties. The rule allows partial claims where specific business portions can be identified and properly documented.

Sole trader expense apportionment HMRC requirements demand accurate calculation and supporting evidence. Mixed-use expenses require careful analysis to separate business and personal elements.

3-step compliance framework

- Identify mixed-use expenses

- Apply reasonable apportionment methodology

- Retain supporting digital evidence

Practical Examples of Mixed-Use Expense Apportionment

Example 1 – Home office (sole trader)

A freelancer using one room of a 4-room property may apportion utilities using room basis and time usage. A typical method is 1/4 rooms × business hours proportion.

Example 2 – Vehicle usage

A consultant driving 8,000 business miles out of 12,000 total annual miles must restrict claims to documented business journeys only. Mileage logs become critical evidence.

Example 3 – Mobile phone

Where a phone is used for both personal and business communication, many accountants apply a reasonable percentage based on call patterns rather than claiming full cost.

Practitioner Insight: Why HMRC Is Focusing on Expense Behaviour

UK accountants increasingly observe that incorrect expense claims rarely stem from deliberate fraud but from misunderstanding mixed-use rules. HMRC’s digital prompts aim to change taxpayer behaviour earlier in the filing process rather than relying solely on post-submission enquiries.

In practice, advisers often see recurring issues in:

- Home office cost over-allocation

- Vehicle fuel claims without mileage evidence

- Subscription tools with partial business relevance

- Property expenses incorrectly treated as repairs

What is the impact on Sole Traders?

Let us understand that what is the impact of this on the sole traders specifically:

Common expense claim errors

Sole traders frequently miscategorise personal expenditure as business costs. Clothing purchases represent a typical problematic area. Clothing that is worn both in work and out of work obviously has a dual purpose and so no deduction is allowed.

What expenses can sole traders claim for tax relief in 2026 remains unchanged fundamentally. However, evidence requirements have increased significantly. HMRC expects detailed justification for all claims.

Equipment purchases require careful consideration of business use. Laptops, phones, and tools used personally cannot claim full relief. Apportionment becomes mandatory for mixed-use items.

Enhanced record keeping requirements

HMRC is now accelerating its MTD programme throughout 2025, 2026 and 2027, with landlords, self-employed individuals and sole traders firmly in its sights. Making Tax Digital creates additional compliance obligations.

Simplified expenses HMRC 2025 options remain available for qualifying taxpayers. However, detailed records still support these simplified calculations. HMRC can request underlying documentation during enquiries.

Digital record-keeping becomes mandatory from April 2026 onwards. Self-Assessment filing deadlines 2025 remain unchanged, but preparation requirements increase. Compatible software must maintain comprehensive expense tracking.

Penalty implications

Incorrect expense claims trigger automatic penalties. The severity depends on the amount and intent:

- Careless errors: 15–30%

- Deliberate concealment: 70–100%

Source: GOV.UK – Penalties for inaccuracies

Landlord Tax implications

Here are the implications of tax which will be applied on the landlords:

Property expense apportionment

Where a property serves as both a rental and personal residence, landlords must split expenses accurately.

Capital vs revenue

Capital improvements (upgrades, extensions) must be depreciated.

Revenue expenses (like-for-like repairs) can be claimed immediately.

| Property Expense Type | Tax Treatment | Evidence Required |

| Like-for-like repairs | Revenue (immediate relief) | Invoices, before/after photos |

| Improvements | Capital (depreciation) | Planning permissions, specifications |

| Maintenance contracts | Revenue (apportioned) | Service agreements, usage logs |

| Utilities | Revenue (apportioned) | Bills, meter readings, occupancy records |

Maintenance & Repair considerations

Landlords must distinguish between allowable repairs and personal improvements. Replacing like-for-like items typically qualifies as revenue expenditure. Upgrades and enhancements usually represent capital improvements.

Mixed-use properties complicate expense allocation further. Landlords living in part of rental properties need detailed apportionment. Room counts, floor areas, and usage time all influence calculations.

| Property Expense Type | Tax Treatment | Evidence Required |

|---|---|---|

| Like-for-like Repairs | Revenue (immediate relief) | Invoices, before/after photos |

| Property Improvements | Capital (depreciation) | Planning permissions, specifications |

| Maintenance Contracts | Revenue (apportioned) | Service agreements, usage logs |

| Utilities | Revenue (apportioned) | Bills, meter readings, occupancy records |

How to avoid HMRC penalties for personal expense claims in 2026?

Proactive compliance measures reduce penalty risk and enquiry likelihood:

- Review 2024/25 and 2025/26 expense claims and remove personal elements.

- Keep receipts, invoices, and clear apportionment calculations.

- Maintain a mileage log with date, journey, purpose, and miles.

- Consider voluntary disclosure if past returns contained errors.

Risk Indicators That May Trigger HMRC Review

- Large year-on-year expense fluctuations

- High home office ratios

- Vehicle costs inconsistent with turnover

- Significant mixed-use equipment claims

- Repeated amendments after submission

Action steps for Compliance

Immediate Actions

- Review 2024/25 tax return preparations

- Identify any personal elements in business expense claims

- Gather supporting documentation for all apportionments

Ongoing Measures

- Implement robust record-keeping systems

- Apply consistent apportionment methodologies

- Consider voluntary corrections for previous years if necessary

Technology & Digital solutions

HMRC’s digital transformation includes enhanced compliance monitoring systems. Automated checks identify unusual expense claiming patterns across taxpayer groups. The new online services will integrate expense monitoring capabilities.

Compatible software solutions help maintain accurate records and calculate apportionments correctly. Many systems now include HMRC-recognized features for expense categorization and documentation.

Businesses uncertain about expense categorisation often benefit from structured bookkeeping processes, which help ensure Self-Assessment data remains evidence-ready throughout the year.

When Should You Seek Professional Advice?

Consider professional support where:

- Multiple mixed-use assets exist

- Property and trading income overlap

- Historic expense treatment may require correction

- MTD transition is approaching

- Time constraints prevent detailed record maintenance

Professional Support & Resources

Qualified tax advisers can assist with complex apportionment calculations and compliance requirements. Professional guidance helps navigate the updated HMRC guidelines and avoid common pitfalls. Investment in professional advice often prevents costly penalties and enquiry procedures.

HMRC provides guidance documents and online resources explaining expense rules and apportionment requirements. Regular updates reflect changes in compliance focus and acceptable practices.

Common mistakes to avoid

Here are some of the common mistakes took place by many, keep a list of these handy so that you do not commit any of these:

Frequent classification errors

Personal credit card payments for business expenses create confusion. Proper documentation must separate business elements from personal spending. Mixed transactions need detailed breakdown and justification.

Subscription services serving dual purposes require careful handling. Software used for both business and personal activities needs apportionment. Netflix subscriptions rarely qualify for business deductions.

Travel expenses combining business and personal elements face scrutiny. Conference attendance with holiday extensions needs careful splitting. Hotel costs, meals, and transport require separate analysis.

Record keeping failures

Inadequate supporting documentation undermines legitimate expense claims. HMRC expects comprehensive evidence for all claimed amounts. Missing receipts result in disallowed deductions and potential penalties.

Timing issues affect expense validity under accruals accounting. Pre-trading expenses need special treatment and documentation. Post-cessation costs rarely qualify for business relief.

Bank statement entries alone provide insufficient evidence. Additional documentation proving business purpose becomes essential. Purpose, date, amount, and business rationale need clear demonstration.

How to prepare for HMRC Enquiries?

Here are some of the ways using which you can prepare for HMRC enquiries:

Enquiry triggers & warning signs

Digital campaign algorithms identify potential compliance risks automatically. Significant year-on-year expense variations trigger additional scrutiny. Industry benchmarking highlights unusual expense patterns.

HMRC expense enquiry 2025 investigations focus on high-risk areas. Home office claims exceeding reasonable proportions attract attention. Vehicle expenses inconsistent with business scale raise flags.

Professional indemnity insurance claims may indicate compliance problems. HMRC cross-references professional advice costs with enquiry outcomes. High advisory costs sometimes suggest underlying issues.

Response strategies

Prompt response to HMRC enquiries demonstrates cooperative attitude. Complete documentation packages support expense claim validity. Professional representation helps navigate complex enquiry processes.

Voluntary disclosure of errors shows willingness to comply. Self-correction often reduces penalty percentages significantly. Early engagement prevents enquiry escalation problems.

Settlement negotiations may resolve enquiries more efficiently. Professional advice guides optimal resolution strategies. Cost-benefit analysis influences negotiation positions.

Official resources for further reading

- HMRC: Self-employed expenses

- HMRC: Making Tax Digital for Income Tax

- HMRC Business Income Manual – Wholly & Exclusively Rule

- GOV.UK: Penalties for inaccuracies

- ICAEW: HMRC targets personal expenditure

Conclusion

HMRC’s enhanced focus on personal expenses requires immediate attention. Self-Assessment filing cycles now operate under increased digital scrutiny, making accurate expense classification more important than ever. Proactive compliance helps prevent avoidable enquiries, adjustments, and penalties.

Digital transformation is reshaping record-keeping expectations across sole traders, landlords, and self-employed professionals. With Making Tax Digital approaching, early adoption of structured bookkeeping processes can significantly reduce compliance risk.

Professional support also becomes increasingly valuable under enhanced monitoring. Specialist guidance helps businesses apply correct apportionment methods, maintain evidence, and respond confidently to HMRC queries.

Ultimately, penalties for incorrect expense claims can escalate quickly without proper controls. Establishing consistent processes, maintaining documentation, and reviewing expense treatment regularly provides a sustainable and low-risk compliance approach.

Frequently Asked Questions

What counts as personal expenditure under HMRC rules?

Personal expenditure includes costs that provide a private benefit rather than being incurred wholly and exclusively for business purposes. Common examples include everyday clothing, personal meals, private travel, and household expenses unrelated to business activity. HMRC applies the wholly and exclusively rule strictly when assessing allowable deductions.

Can I apportion mixed-use expenses for tax relief?

Yes. Where an expense has both personal and business use, only the identifiable business portion can be claimed. HMRC expects a reasonable and consistent apportionment method supported by calculations and evidence, such as usage logs, time analysis, or mileage records.

What records do I need to support expense claims?

You should maintain receipts, invoices, bank transaction evidence, and notes explaining the business purpose of each expense. For mixed-use items, documentation must also show how the business portion was calculated. Digital records with timestamps strengthen audit readiness.

What penalties apply under HMRC’s expense compliance campaign?

Penalties depend on behaviour and accuracy. Careless errors typically result in penalties of 15–30% of the additional tax due, while deliberate inaccuracies can lead to penalties of up to 100%. Correcting errors voluntarily before HMRC intervention can significantly reduce penalties.

When do the new digital record-keeping requirements start?

Making Tax Digital for Income Tax is scheduled to begin from 6 April 2026 for eligible taxpayers. This will introduce quarterly digital reporting and require compatible software to maintain business income and expense records.

Does receiving an HMRC expense email mean an investigation has started?

No. Most HMRC emails related to expenses are behavioural prompts designed to encourage accurate reporting. However, repeated warnings, inconsistencies, or significant discrepancies may increase the likelihood of a formal enquiry.

What percentage of home expenses can sole traders claim?

There is no fixed percentage allowed by HMRC. Claims must be based on a reasonable method, such as room usage, time spent working from home, or actual cost analysis. The approach should be consistent and supported by evidence.

Will HMRC check past years’ expense claims?

Yes. HMRC can review earlier returns where patterns suggest persistent errors or where corrections materially affect tax liability. Maintaining historical documentation and applying consistent treatment helps reduce risk during retrospective checks.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.