Tax code 1257L is the code HMRC currently uses for most people who have one job or pension. It generally means your employer is applying the standard Personal Allowance through PAYE. For the 2026/27 tax year, the standard Personal Allowance is £12,570.

However, a payslip does not confirm whether that code still matches your circumstances. Starting a new job, receiving a benefit that hasn’t been reported, or taking on a second income can all mean 1257L is no longer the correct tax code..

This guide explains what 1257L means, who usually receives it, how it affects pay through the Personal Allowance and what happens once income exceeds £100,000.

Key takeaways

- 1257L gives a tax-free Personal Allowance of £12,570 for 2026/27, unchanged since 2021/22.

- The letter “L” indicates you’re entitled to the standard Personal Allowance.

- Once income exceeds £100,000, the Personal Allowance is reduced by £1 for every £2 earned, and it is removed entirely at £125,140.

- The allowance freeze now runs until April 2031, so more pay is taxed each year even without any rate changing.

What does Tax Code 1257L mean in the UK?

For most employees, 1257L simply means the standard Personal Allowance is being applied through PAYE.

The code combines a number and a letter, with each serving a different purpose when calculating how much tax should be deducted. The number 1257 represents a tax-free Personal Allowance of £12,570 for the 2026/27 tax year.

The letter “L” indicates entitlement to the standard Personal Allowance. The “1257” part reflects the standard allowance (£12,570) with the last digit removed.

That combination is what makes 1257L the standard code: an employer deducts tax only on pay above £12,570, spread evenly across the year rather than recalculated each pay period.

How 1257L works on your Pay in 2026/27?

1257L does not just confirm a tax-free amount. It determines which portion of your pay is taxed, at what rate and when. The bands apply in order from the bottom up. Each tax rate applies only to the portion of income within that band, not to your total earnings.

| Income Band | Tax Rate | What it means |

|---|---|---|

| Up to £12,570 | 0% | Tax-free Personal Allowance under 1257L |

| £12,571 to £50,270 | 20% | Basic rate applies to income in this band |

| £50,271 to £125,140 | 40% | Higher rate applies to income in this band |

| Above £125,140 | 45% | Additional rate applies, Personal Allowance is zero |

Example (straightforward case with the standard Personal Allowance and no adjustments): someone earning £30,000 pays no tax on the first £12,570. The remaining £17,430 is taxed at 20%, resulting in £3,486 in income tax for the year. The full £30,000 is never taxed as a single figure.

Note: Scottish taxpayers pay income tax under different bands. The same £12,570 allowance applies but the rates above it differ.

Who is given 1257L and who isn’t?

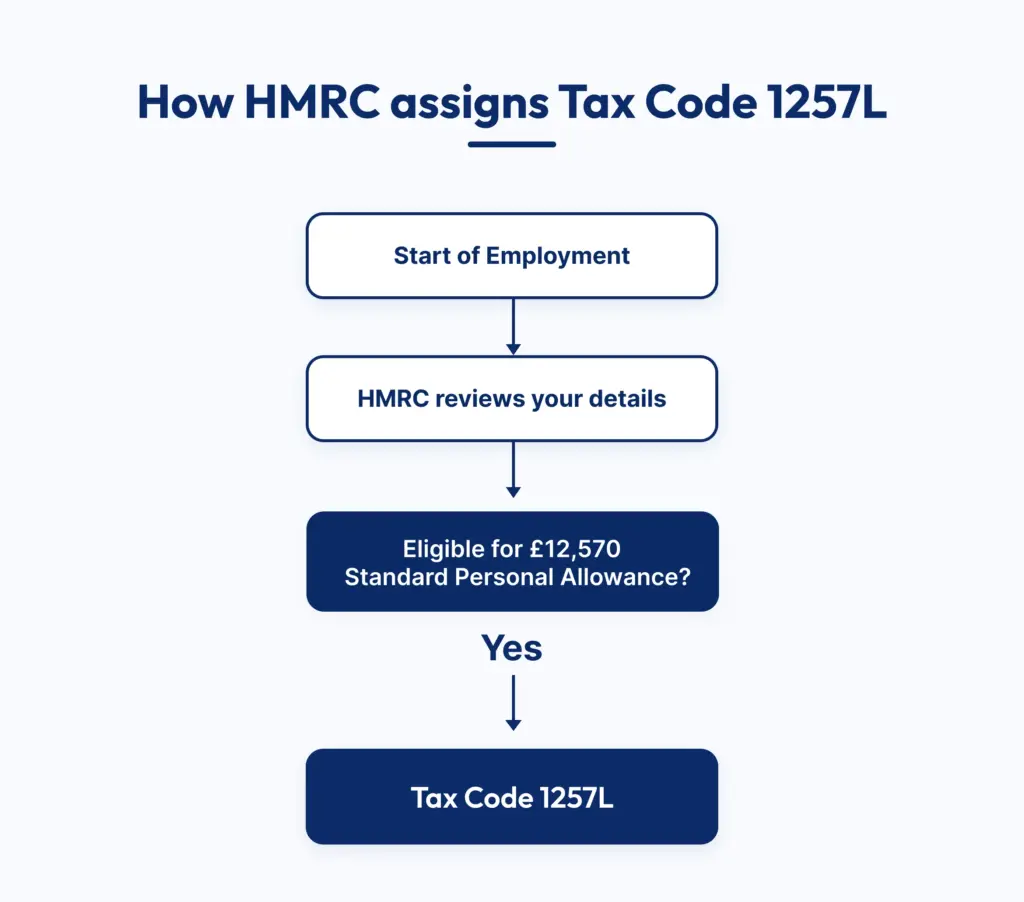

Anyone with a single job or pension and no other income or benefit affecting their tax position, is usually placed on 1257L automatically.

HMRC does not assign tax codes randomly. It reviews information from your employer, pension provider and previous tax records to decide whether you are entitled to the standard Personal Allowance. For most people with one source of income and no adjustments, this results in the 1257L tax code.

However, the standard 1257L code only applies while nothing affects your tax position. If HMRC records any adjustment, it may replace 1257L with another tax code.

- More than one job or pension is being paid at the same time

- A benefit applies, such as a company car or private medical cover

- Unpaid tax from an earlier year is being collected through the current code

- Marriage Allowance has been given to or received from a spouse or civil partner

- Starter details were missing when the job began

None of these correct themselves the moment they happen. A benefit that begins or a second income that starts, only changes the code once HMRC has been told and the code stays exactly where it was until that step happens.

How the Personal Allowance reduces above £100,000?

Once income passes £100,000, the £12,570 allowance no longer stays fixed. GOV.UK’s page on current Income Tax rates and Personal Allowances confirms it starts reducing by £1 for every £2 earned above that threshold.

How the reduction works

For every £2 earned past £100,000, £1 is removed from the £12,570 allowance. Earning £10,000 over the threshold removes £5,000 from the allowance, leaving £7,570 tax-free instead of the full amount. The allowance continues reducing as income rises further, until it reaches zero entirely at £125,140.

Why this band is taxed more heavily than it looks

Between £100,000 and £125,140, two things happen together: income in this band is already taxed at 40% and the allowance is being withdrawn at the same time.

Because the Personal Allowance is reduced as income rises above £100,000, the amount of income taxed at higher rates increases in this band.

The frozen allowance and its effect on pay

The £12,570 allowance has not moved since 2021/22. The House of Commons Library notes that the Personal Allowance has been fixed since 2021/22 and is due to remain at this level until 2030/31.

Pay continues to rise with inflation, but the allowance does not, so a growing portion of income each year lands in a taxed band rather than the tax-free one, without a single rate actually changing.

The impact is gradual rather than immediate. As earnings increase while the allowance stays fixed, a larger share of income becomes taxable even though the tax rates themselves do not change.

Conclusion

For most employees, 1257L simply means the standard Personal Allowance is being applied through PAYE. However, changes to income, benefits or employment circumstances can affect whether that code remains appropriate.

Understanding how the code works, particularly how the Personal Allowance changes above £100,000, makes it easier to understand the tax deducted from your pay.

Outbooks works with UK employers on payroll accuracy, including tax code checks across new starters, benefits and second incomes. Call +44 330 057 8597 or email info@outbooks.co.uk to have a payroll reviewed.

FAQs

What is the difference between 1257L and 1257L M1, W1 or X?

1257L applies the allowance across the full year, while M1, W1 and X apply it separately to each pay period. The emergency versions are usually temporary, used until HMRC has an employee’s complete starter details.

Why would a tax code change during the year?

A code updates whenever HMRC learns of a change, such as a new job, a benefit starting, an unreported second income or a correction linked to unpaid tax from an earlier year.

Does self-employment income change a PAYE tax code?

It can, where the extra income affects the overall tax owed. HMRC may adjust the code so part of that tax is collected through PAYE instead of through a Self Assessment bill.

What happens to the allowance above £100,000?

It reduces by £1 for every £2 earned over £100,000, reaching zero once income hits £125,140, so the full £12,570 allowance no longer applies past that point.

Why is a second job taxed differently to a first?

The Personal Allowance usually sits against one job only, so a second job is commonly taxed under BR, D0 or D1, with no allowance applied against that income at all.

What does the S or C prefix on a tax code mean?

An S prefix means Scottish Income Tax rates apply and a C prefix means Welsh rates apply. Both still use the same £12,570 allowance, just under different tax bands.

Can a tax code fall instead of rise?

Yes, a falling code usually points to a benefit in kind or unpaid tax being collected through the code, rather than any change to the Personal Allowance figure itself.

Does a tax code reset automatically every 6 April?

Not unless HMRC or an employer has a specific reason to update it. Without a reported change, the same code typically carries into the new tax year unchanged.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.