Employers who provided taxable benefits during 2025/26 must submit P11D forms to HMRC by 6 July 2026. A late P11D(b) results in automatic monthly penalties.

HMRC can charge penalties for inaccurate P11D returns and in serious cases, penalties of up to £3,000 per form may apply depending on the nature of the error and the circumstances involved.

The errors that lead to those penalties are rarely complex. Incorrect company car data, missing benefit entries, incomplete P11D(b) submissions and confusion around payrolled benefits account for the majority of P11D compliance failures each year.

This guide covers where those mistakes occur, what HMRC charges when they do, how to correct a return already submitted and what to check before the deadline.

Key takeaways

- P11D and P11D(b) forms for 2025/26 must be submitted by 6 July 2026; employees must also receive their P11D copies by that date.

- Class 1A NIC for 2025/26 is charged at 15% and must be paid by 22 July 2026 for electronic payments or 19 July for cheque.

- HMRC can charge up to £3,000 per incorrect P11D form; the amount scales based on whether the error was careless or deliberate.

- A late P11D(b) generates an automatic penalty of £100 per 50 employees per month until it is filed.

- All P11D amendments must be submitted online; HMRC does not accept paper corrections.

- An error corrected before HMRC raises it will always carry a lower penalty than one corrected after.

Common P11D Filing mistakes and how to avoid them

P11D errors repeat across employers year after year. Each of the mistakes below includes a direct fix so the issue can be addressed before submission.

Incorrect company car and fuel benefit data

The taxable value of a company car depends on its list price, CO₂ emissions band, fuel type and the exact dates it was available to the employee. Using last year’s emissions figure without checking for updates, applying the wrong percentage or omitting fuel benefit when private fuel was provided all affect the final value reported to HMRC.

Availability dates must also be accurate. If a car was available for the full tax year, the “from” date must be completed with the “to” date left blank. If both dates are left blank, HMRC processes the entry as incomplete.

Fix: Check CO₂ emissions and list price against current HMRC approved figures before filing and confirm availability dates against employment records for every car on the return.

Reporting exempt or payrolled benefits incorrectly

Not all employee benefits need to be reported on a P11D. You can exclude a benefit under the trivial benefits exemption if it meets all of the following conditions:

- It costs £50 or less to provide.

- It is not cash or a cash voucher.

- It is not in the terms of the employee’s contract.

- It is not a reward for their work or performance.

If a benefit meets all four conditions, it does not need to be included on a P11D.

Any benefit an employer has registered to payroll through PAYE must not also appear on the P11D. Reporting a benefit in both places creates a double charge: the employee pays tax through payroll and again through a tax code adjustment.

Fix: Cross-reference your payrolled benefits register against the P11D before submission and remove any item already processed through PAYE.

Incomplete P11D entries

Each benefit section on the P11D requires specific information depending on the type of benefit being reported. Missing figures or incomplete entries can result in incorrect reporting and may lead to HMRC queries or amendments.

For P11D private medical insurance, the reportable figure is the employer’s premium cost not the value of any claim made by the employee.

Fix: Check every benefit entry has both the cost and cash equivalent fields completed before submitting.

Incorrect benefit valuations on P11D forms

Benefits must be reported at their correct taxable value, not at cost to the employer. Two benefits where employers most often get the valuation wrong are living accommodation and beneficial loans.

For living accommodation, the basic benefit is based on the property’s annual value, not the rent the employer pays. For properties that cost more than £75,000, an additional charge also applies. Use the P11D working sheet on GOV.UK to arrive at the correct cash equivalent figure.

For beneficial loans, the taxable value is based on HMRC’s official rate of interest. The official rate of 3.75% from 6 April 2025 is confirmed in HMRC’s Employment Income Manual.

Fix: Confirm the official rate from HMRC’s beneficial loan rates guidance. The rate for the 2025/26 tax year was 3.75%. Also use the P11D accommodation working sheet for living accommodation calculations.

Taxable benefits omitted from the return

Employer-paid professional subscriptions where the body is not on HMRC’s approved List 3 and relocation costs above the £8,000 exemption threshold are commonly missed. HMRC cross-references employer spending data with P11D submissions, making omissions a common reason for a compliance check.

Fix: Run through HMRC’s full expenses and benefits A to Z and check each category against what was provided to employees during 2025/26.

P11D errors on individual forms are one part of the picture. The P11D(b) carries its own obligations and its own separate penalty structure.

P11D(b): Separate Obligations and Penalties

The P11D(b) must be filed if you submitted any P11D forms, paid expenses through payroll or received a notice from HMRC to file. An employer who did none of these and has no Class 1A NIC liability does not need to file one. Where HMRC has previously issued a P11D(b) notice, confirm your nil position in writing to avoid an automatic penalty.

Where individual P11D corrections change the total benefit value, the P11D(b) must also be resubmitted. An uncorrected P11D(b) left in place while individual forms are amended creates a discrepancy HMRC will identify during processing.

| Error | What goes wrong | Consequence |

|---|---|---|

| Not filing a P11D(b) at all | Employer assumes it is only needed when NIC is owed | Automatic monthly penalty regardless of intent |

| Filing with incorrect totals | P11D corrections not carried through to P11D(b) | Class 1A NIC underpayment; interest accrues from 22 July |

| Missing the filing deadline | P11D(b) submitted after 6 July 2026 | £100 per 50 employees per month until filed |

| Late NIC payment | Class 1A NIC not paid by 22 July 2026 | 5% surcharge applies if unpaid 30 days after the due date, a further 5% if still unpaid at 6 months and a further 5% at 12 months |

Understanding what HMRC charges for each type of error determines how urgently corrections need to be made.

What are the HMRC Penalties for P11D mistakes?

HMRC penalties for P11D errors cover two separate areas: penalties for a late or missing P11D(b) and penalties for inaccurate figures on individual P11D forms. The two are charged independently a correctly filed P11D(b) does not offset a penalty for an incorrect P11D.

Late P11D(b) Penalties

HMRC charges an automatic penalty of £100 for every 50 employees, or part thereof, for each complete or partial month a P11D(b) remains unfiled after 6 July 2026. An employer with 105 employees faces £300 per month until the form is submitted.

This penalty cannot exceed the total Class 1A NIC due for the year and where it would otherwise total less than £100, HMRC does not charge it.

A further surcharge applies to unpaid Class 1A NIC. If the amount owed is not paid by 22 July 2026, a further 5% surcharge is added 30 days after that date. A further 5% applies if the amount remains unpaid at six months, and a further 5% at 12 months, with interest running separately from 22 July.

Incorrect P11D Penalties

Where HMRC finds that a P11D contains errors, it can charge up to £3,000 per form. The actual amount scales according to the behaviour behind the error and whether the employer corrected it voluntarily or only after HMRC raised the issue.

The ranges below reflect HMRC’s standard inaccuracy penalty framework and the final penalty depends on the nature of the error, the behaviour involved and whether the disclosure was prompted or unprompted.

| Behaviour | Voluntary disclosure | Prompted by HMRC |

|---|---|---|

| Careless | 0% to 30% | 15% to 30% |

| Deliberate, not concealed | 20% to 70% | 35% to 70% |

| Deliberate and concealed | 30% to 100% | 50% to 100% |

A careless error such as using an unchecked prior year figure or applying the wrong emissions band involves a 0% penalty where the employer identifies and corrects it before HMRC raises the issue.

These penalties apply in addition to any interest charged on unpaid Class 1A NIC from 22 July 2026. Where an error has already been submitted, the correction process is direct.

How to Amend a P11D after Filing?

Since 6 April 2023, all P11D corrections must be submitted online. HMRC does not accept paper amendments except from employers who have stopped trading.

Two correction forms are available on GOV.UK:

- P11D correction form to correct benefit figures for individual employees

- P11D(b) correction form to revise the total Class 1A NIC where corrected figures affect the overall liability

Once the correct form has been identified, the correction itself follows a fixed sequence.

Each of these steps is explained in detail below.

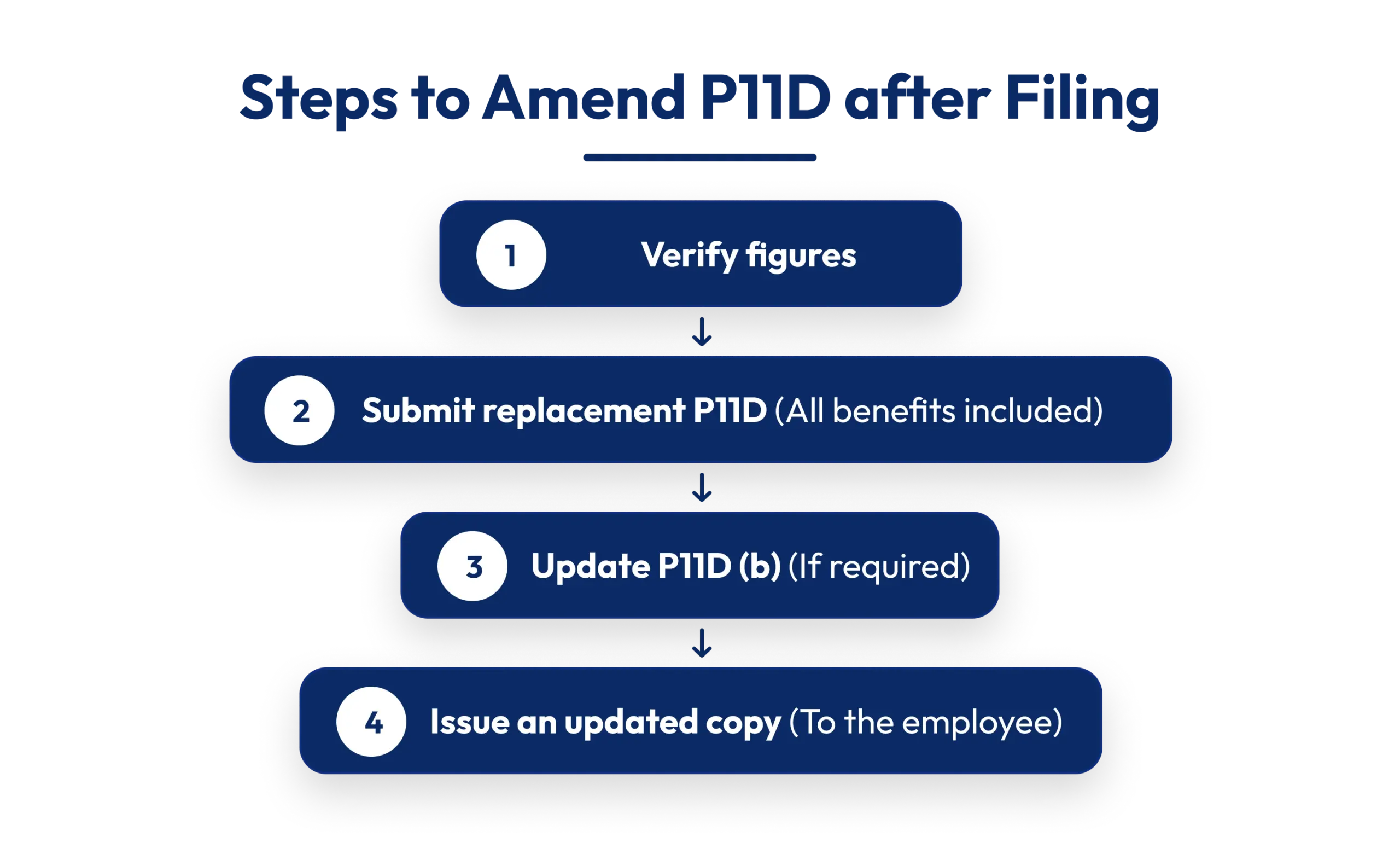

Step 1: Confirm the correct figures for every benefit on the affected employee’s return before starting.

Step 2: Submit a full replacement P11D. All benefits for that employee must be included not only the item being corrected.

Step 3: If the correction changes the total Class 1A NIC owed, submit an amended P11D(b) showing the full revised total not the difference from the original. Pay any additional NIC promptly to limit interest.

Step 4: Send the employee an updated P11D copy confirming it replaces the earlier version. Where they file a self-assessment return, they may need to update it using the corrected figures.

For example: if a P11D was submitted with a medical benefit entered at £300 but the correct figure is £500, the replacement form must include the corrected medical figure alongside every other benefit on that employee’s return. Submitting only the amended item is not accepted by HMRC.

What can be amended online:

The online correction form covers:

- Company car and fuel benefit values

- Private medical insurance premiums

- Beneficial loan interest calculations

- Exempt benefits that were incorrectly included

- Benefits reported twice due to payrolling overlap

What requires a different route:

- Errors from failing to register for payrolling benefits correctly require direct contact with HMRC

- Where liabilities span multiple earlier tax years, a voluntary disclosure and contract settlement with HMRC is the appropriate route

HMRC assessment time limits:

There is no fixed date for submitting a P11D correction. HMRC’s assessment time limits apply to how far back it can raise a charge if it identifies the error first:

- 4 years: where no careless or deliberate behaviour is involved

- 6 years: careless errors

- 20 years: deliberate errors

The longer an error remains uncorrected, the greater the interest and penalty exposure. The pre-submission checklist below covers the checks that prevent most of these corrections from being needed at all.

Pre-Submission Checklist for 2025/26

Before submitting P11D and P11D(b) forms, confirm the following:

- A P11D has been prepared for every employee who received a taxable benefit during 2025/26

- Company car data list price, CO₂ band, fuel type and availability dates has been checked against current records

- No payrolled benefits have been included on the P11D

- Trivial benefits under £50 that meet the exemption criteria have been excluded

- The cash equivalent box is completed for every benefit entered

- Living accommodation values use the correct annual value method

- Beneficial loan interest has been calculated using the official rate of 3.75% for 2025/26

- The P11D(b) total matches the sum of all individual P11D figures

- Class 1A NIC payment is scheduled for no later than 22 July 2026

- Employees will receive their P11D copies by 6 July 2026

What changes when P11D work is Outsourced?

P11D errors in practice rarely come from not knowing the rules. They come from processing a high volume of data car figures, insurance premiums, loan balances and availability dates across multiple employees under deadline pressure with limited time for verification.

A single overlooked CO₂ band update across one client’s company car fleet means multiple replacement forms, corrected employee copies, a revised P11D(b) and potential interest on underpaid Class 1A NIC. For a practice managing 15 clients with 5 to 20 benefit recipients each, that risk multiplies across every submission window.

Outbooks works with accounting practices and business owners to manage P11D preparation and submission, with verification checks built into the process to identify errors before they reach HMRC. This covers benefit valuation reviews, cross-checking payrolled benefits against P11D entries, P11D(b) reconciliation and deadline management across the full client base.

Conclusion

The errors that result in HMRC penalties incorrect car data, missed benefit entries, incomplete P11D(b) submissions and double-reported payrolled benefits are avoidable in most cases. A careless error corrected before HMRC raises it carries a 0% penalty. The same error corrected after HMRC intervenes carries a minimum of 15%.

With the 6 July 2026 deadline approaching, the priority is to check submissions before filing and correct any errors already submitted as soon as possible. For accounting practices and employers where P11D volume creates consistent compliance risk, working with a specialist removes that exposure at source.

For P11D preparation and compliance support for the 2025/26 tax year, contact Outbooks at +44 330 057 8597 or info@outbooks.co.uk.

Frequently Asked Questions

What is the P11D deadline for the 2025/26 tax year?

P11D and P11D(b) forms must be submitted to HMRC by 6 July 2026. Employees must receive their individual P11D copy by the same date. Class 1A NIC is due by 22 July 2026 for electronic payments and 19 July 2026 for cheque payments.

Do I need to file a P11D(b) if no benefits were provided?

No P11D(b) is required if no employees received taxable benefits and no Class 1A NIC is owed. If HMRC has previously received a P11D(b) from your organisation, confirm your position in writing to avoid automatic penalty notices.

What is the maximum penalty for an incorrect P11D?

HMRC can charge up to £3,000 per incorrect P11D form. The amount depends on whether the error was careless or deliberate and whether the employer corrected it before or after HMRC raised the issue.

Can a P11D be corrected after it has been submitted?

Yes, but only online via GOV.UK. A full replacement P11D is required for the affected employee partial corrections are not accepted. If the correction changes the Class 1A NIC total, the P11D(b) must also be resubmitted showing the full revised amount.

What happens if payrolled benefits are also reported on a P11D?

Reporting a benefit through payroll and on a P11D creates a double charge. The employee is taxed through payroll and again through a tax code adjustment. Any benefit already processed through PAYE must be excluded from the P11D entirely.

How far back can HMRC investigate P11D errors?

For errors with no careless or deliberate behaviour, HMRC can assess up to 4 years back. For careless errors, the limit is 6 years. For deliberate errors, HMRC can investigate up to 20 years.

What is a contract settlement with HMRC?

A contract settlement resolves unpaid tax liabilities including those from P11D errors through a negotiated agreement with HMRC. It covers tax, NIC, interest and penalties in one arrangement and typically produces a lower penalty outcome than a correction made after HMRC has opened an enquiry.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.