FULL EXPENSING

Among the announcements in the Spring Budget, UK chancellor Jeremy Hunt has introduced full expensing as a successor to the super-deduction tax break.

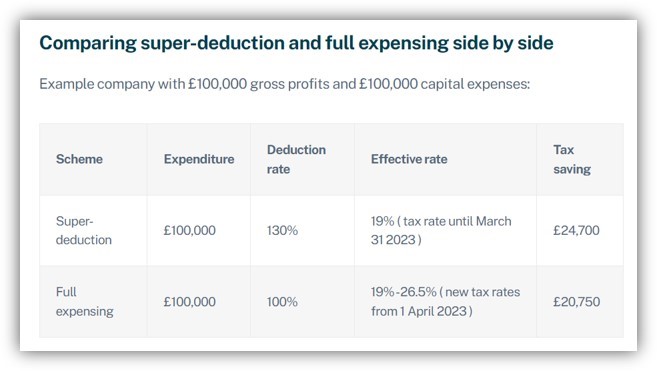

The UK government will replace the super-deduction tax relief scheme with the three-year full expensing regime from 01 April 2023.

Full expensing will allow businesses across the UK to write off the full cost of qualifying plant and machinery investment in the year they invest. It can be deducted “in full and immediately” from taxable profits. It is effective from 01 April 2023 to 31 March 2026.

Equipment includes but is not limited to:

- Warehousing equipment such as forklift trucks

- Tools such as ladders and drills

- Construction equipment such as bulldozers and excavators

- Machines such as computers and printers

- Office equipment such as chairs and desks

- Some fixtures such as kitchen and bathroom fittings

- Fire alarm systems

Full expensing is available to companies subject to corporation tax only. Unincorporated businesses cannot claim, but such businesses are entitled to claim the Annual Investment Allowance (AIA), which offers the same benefits as full expensing for the investments it covers (up to £1m per year).

Why has it been introduced?

Full expensing has been introduced to encourage UK companies to invest more in modern plant, tools, machinery, and technology. In 2021 for example, UK business investment accounted for 10.0% of GDP compared to an average of 12.5% among our overseas competitors.

An example of full expensing

A company has gross annual profits of £10 million in the 2023-24 tax year. Instead of paying corporation tax of £2,500,000 on this sum, the business invests in a new state-of-the art production line, spending £10 million on various items of main rate plant and machinery.

The company can claim £10 million under full expensing in the year the expenditure is incurred, so they deduct the whole sum from their gross profits, reducing their corporation tax bill to zero. The £2,500,000 they would have paid in tax is now set against the cost of the production line, reducing the real expense by 25% to £7,500,000.

What if my profits are too low or I’ve made a loss?

Under full expensing you can only claim against your pre-tax profits. If the value of the assets you have bought are higher than your profits, or you have zero profits because you have made a loss, you can set part of the asset cost against whatever profits you have. The balance of the value of the asset can then be rolled over and set against profits, using full expensing, in the next tax year, or any tax year until the scheme ends in March 2026. (The government has said they may consider making full expensing permanent at a later stage and before the expiry point).

Can I utilise full expensing if I’m in a partnership?

No, full expensing is only open to incorporated businesses that pay corporation tax.

Can a sole trader utilise full expensing?

No, full expensing is not available to sole traders, partnerships, or LLPs. It’s only open to incorporated businesses that pay corporation tax. However, non-eligible businesses are still entitled to claim the Annual Investment Allowance (AIA) which offers the same benefits as full expensing for the investments it covers (up to £1 million per year).

Is my business eligible?

Your business is eligible if it’s an incorporated company and it spends money on any of the qualifying plant and machinery listed above.

What happens if I sell the asset/s?

When a company sells an asset on which it has claimed full expensing, the company will be required to bring in an immediate balancing charge equal to 100% of the disposal value. This means that if the company sold an asset for £10,000 on which they had claimed full expensing, they would be required to increase their taxable profits by a matching £10,000.

What other capital allowances exist in the UK?

As well as full expensing, UK businesses may utilise other forms of capital allowance. These options will be of special interest to non-corporations who cannot claim full expensing.

Other capital allowances include:

- Annual investment allowance (AIA) which allows businesses to claim 100% of the cost of plant and machinery up to £1m in the year it is incurred

- Writing down allowances (WDA) which spread the tax deductions over time at 18% and 6% a year for main rate and special rate expenditure respectively.

- First-year allowances (FYA) which allow a company to claim a percentage of the cost of plant and machinery investments in the year it is incurred.

- Structures and buildings allowances (SBA) which allow a business to deduct 3% per year over 33 1/3 years for qualifying expenditure on non-residential structures and buildings.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.