IR35 does not assess your contract. It assesses how you actually work. A contractor working through a limited company who takes direction from one client, works set hours and cannot genuinely send a substitute is working as an employee in HMRC’s view, regardless of the company structure in place.

From 6 April 2026, the small company thresholds increased. The turnover limit rose from £10.2 million to £15 million. The balance sheet limit rose from £5.1 million to £7.5 million. The 50-employee limit remained unchanged. Around 14,000 companies moved from medium to small, shifting the responsibility back to the contractor’s Personal Service Company (PSC) the limited company through which they provide their services.

Company size is assessed using prior financial year accounts, so for many of those companies the shift in responsibility will only take effect once their status is confirmed based on prior-year accounts, meaning many engagements will continue under the existing rules until April 2027.

Key Takeaways

- IR35 status is tested against three indicators: right of substitution, mutuality of obligation and the degree of control the client exercises.

- If your client is now classed as small, you are responsible for assessing your own status, not the client.

- If you get your status wrong, HMRC can request unpaid tax from previous years, not just the current one.

- For many contractors, this change will not apply until April 2027, as company size is determined using the previous year’s accounts.

- Contractors inside IR35 pay Income Tax and National Insurance as employees but receive no employment rights.

What IR35 is and Who It Applies To?

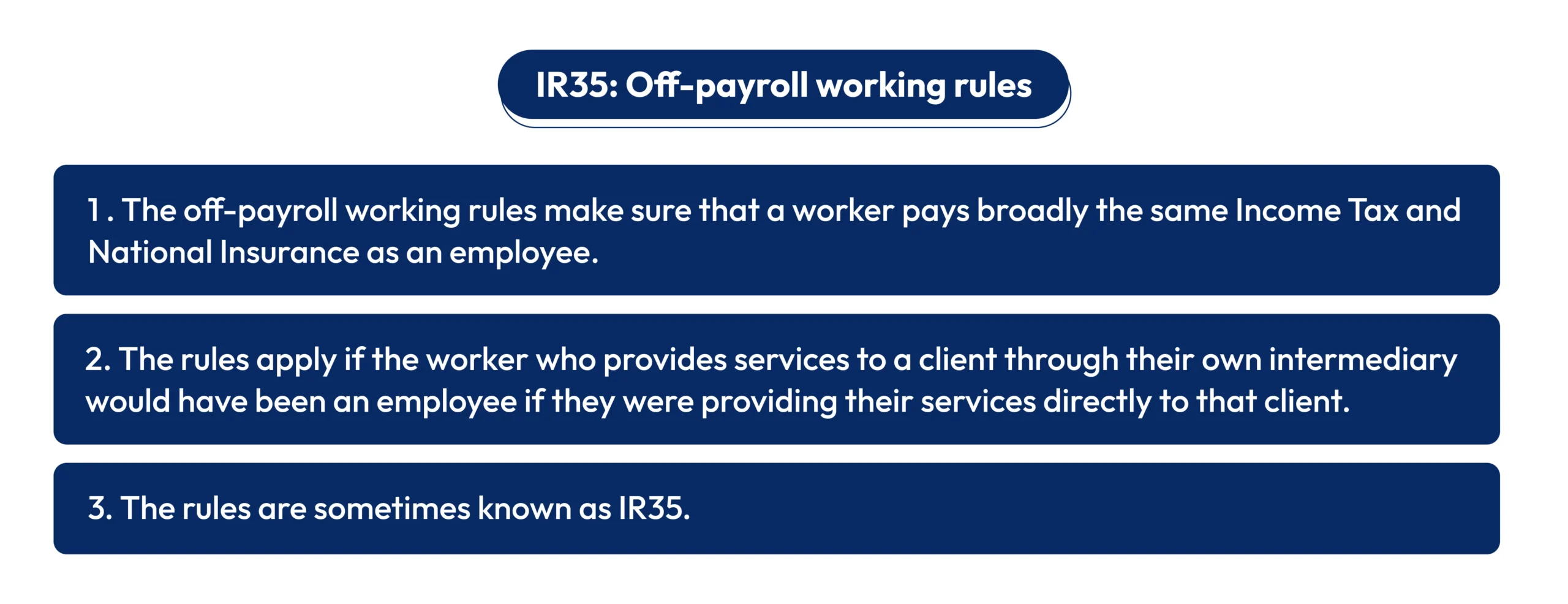

IR35 is HMRC’s legislation for the off-payroll working rules in the UK. It applies when a contractor provides services through a PSC or limited company but would have been classed as an employee had they worked directly for the client. The rules ensure those contractors pay Income Tax and National Insurance on broadly the same basis as employees.

The off-payroll rules apply to all public sector clients and to medium and large private sector clients. Small private sector clients are exempt, meaning the contractor’s PSC determines its own status.

When does it apply:

It applies on a contract-by-contract basis, meaning a contractor can have some engagements inside and others outside. Since the 2021 private sector reforms, HMRC has moved around 120,000 off-payroll workers into deemed employment tax status.

The Three Tests: Right of Substitution, Mutuality of Obligation and Control

IR35 status is assessed against three tests, applied to the working arrangement as it actually exists.

Right of Substitution

The right to send a substitute must be genuine and exercisable. A clause in a contract does not establish the right on its own. If the client controls who performs the work, or if a contractor has worked the same engagement over an extended period without a substitute ever being sent, HMRC will give the clause very little weight.

Mutuality of Obligation

Mutuality of obligation exists where the client is expected to offer work and the contractor is expected to accept it. A contractor who has renewed the same contract repeatedly at the same client, performing the same work, has a strong mutuality of obligation case against them regardless of what the contract states.

Control

Control looks at how, when and where work is carried out. A contractor who attends client premises five days a week, uses client equipment and reports to a line manager is working as an employee in practice.

HMRC’s CEST tool provides a status determination for most engagements and is part of IR35 assessment help available directly from HMRC. Enter details about substitution, control and financial risk and the tool returns a determination. HMRC is bound by the result if accurate information is entered. Retain every output as part of your compliance records.

Inside IR35 and Outside IR35: The Financial Difference

Being inside means Income Tax and National Insurance are deducted before the contractor is paid. Being outside means the contractor pays through their own PSC at a lower effective rate. The table below sets out the key differences.

| Tax and Pay Factor | Inside IR35 | Outside IR35 |

|---|---|---|

| Income Tax | Deducted via PAYE by the fee payer | Paid through self-assessment by the PSC |

| National Insurance | Employee and employer NI both deducted | Lower NI through salary and dividends structure |

| Employment rights | None | None, but greater tax efficiency maintained |

| Who deducts tax | Fee payer, usually the agency or client | Contractor’s own PSC |

How does it affect take-home pay?

When a contractor is inside IR35, the fee payer deducts Income Tax and both employee and employer National Insurance from the assignment rate before paying the contractor. The contractor receives the net amount with no employment rights in return.

Employer National Insurance is also included within the assignment cost and is typically factored into the contractor’s rate, reducing overall take-home pay.

Outside IR35, the full assignment rate is paid to the PSC and the contractor manages their own tax through a more efficient salary and dividends structure.

Who is responsible for Status Decisions?

Responsibility for IR35 status depends on the size and type of the organisation engaging the contractor. The table below reflects the position from 6 April 2026.

| Client type | Who determines the status? | Legislation |

|---|---|---|

| Medium or large private sector | End client issues a Status Determination Statement | Chapter 10 ITEPA 2003 |

| Small private sector | Contractor’s PSC determines its own status | Chapter 8 ITEPA 2003 |

| Public sector, any size | Public body, always responsible | Chapter 10 ITEPA 2003 |

A Status Determination Statement (SDS) is a written document a medium or large client must issue to both the contractor and the fee payer. It must state whether the engagement is inside or outside IR35 and give reasons.

Contractors working with newly reclassified small clients will no longer receive one. Under the off-payroll rules, a contractor can formally request written confirmation of their client’s size. The client has 45 days to respond.

From April 2026, Joint and Several Liability (JSL) rules apply to umbrella company arrangements. Where PAYE is not correctly operated within the labour supply chain, HMRC can recover unpaid tax from other parties, including agencies and, in some cases, end clients. This increases compliance risk and makes due diligence on umbrella companies essential.

Penalties and the PAYE Set-Off Change

Getting IR35 wrong carries direct financial consequences.

- Where a fee payer fails to operate PAYE correctly on an inside engagement, HMRC recovers unpaid Income Tax and National Insurance in full, plus interest.

- Careless errors, where the fee payer was unaware of the inaccuracy, attract a penalty of 30% of unpaid tax.

- Knowingly failing to act on an inside determination carries a penalty of 70% of unpaid tax.

- Actively concealing non-compliance carries a penalty of 100% of unpaid tax.

- Penalties can be avoided entirely where the fee payer can demonstrate they took reasonable care.

- HMRC actively investigates compliance across IT, financial services and oil and gas.

PAYE Set-Off Change

Before 6 April 2024, if a fee-payer got a determination wrong, HMRC pursued the full PAYE and NICs liability with no credit for tax the contractor had already paid through their PSC the same income was effectively taxed twice.

The Finance Act 2024 fixed this. From 6 April 2024, HMRC can offset Income Tax and NICs already paid by the worker and their PSC against the fee-payer’s PAYE liability. The fee-payer pays only the genuine shortfall not the gross amount.

Two important caveats:

- Penalties remain based on the full gross liability. The set-off reduces the bill, not the consequences of getting it wrong.

- Cases settled before 6 April 2024 are not eligible for retrospective relief.

Conclusion

IR35 in the UK applies to working reality, not contract language. The 2026 threshold changes are the most significant development since the 2021 private sector reforms, but the practical effect depends on when a client’s prior year accounts bring them within the new limits. Contractors need written confirmation of their client’s size, a current assessment for each active engagement and documentation to support it.

Accounting firms providing contractor accounting and accountancy for contractors across the reclassified companies need to review each engagement individually. Status, PAYE obligations and self-assessment positions may all have changed.

IR35 compliance requires accurate bookkeeping, PAYE processing and year-end accounting that reflects status correctly. Outbooks works with UK accounting firms and acts as an accountant support partner for contractor clients, handling compliance accurately and on time. Call +44 330 057 8597 or email info@outbooks.co.uk.

Frequently Asked Questions

What is a Status Determination Statement?

A written document a medium or large end client must issue to the contractor and fee payer, stating whether the engagement is inside or outside IR35 and giving reasons.

Can I dispute a status determination?

Yes, raise the disagreement in writing with the end client, stating your reasons. The client must respond within 45 days. If unresolved, refer the matter to HMRC or the Tax Tribunal.

Does IR35 apply if I work through an umbrella company?

No, contractors employed directly by an umbrella company are outside the scope of the off-payroll working rules. It applies specifically to those working through their own PSC or limited company.

What records do I need to keep for IR35 compliance?

Keep all contracts, CEST outputs, Status Determination Statements and any correspondence about working arrangements. These are your primary defence if HMRC raises an enquiry.

What are the penalties for non-compliance?

HMRC recovers all unpaid Income Tax and National Insurance plus interest. Careless errors attract penalties up to 30% of unpaid tax. Deliberate non-compliance can reach 100%.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.