P11D preparation requires employers to identify every reportable benefit-in-kind provided during the tax year, confirm the taxable value for each one and submit accurate returns to HMRC by a fixed deadline. For businesses providing taxable benefits, the records needed to do this are held across payroll, HR and finance.

Most employers know a P11D needs filing. The part that takes time is gathering complete benefit-in-kind records, checking cash equivalent values against HMRC rules and finding reportable benefits that were missed earlier in the year.

This guide covers the common challenges in P11D preparation, how outsourcing can support employers and accounting practices, what to have ready before engaging a provider and what to look for when choosing one.

Key takeaways

- P11D and P11D(b) forms for the 2025/26 tax year must reach HMRC by 6 July 2026, with Class 1A National Insurance contributions due by 19 July (cheque) or 22 July (electronic).

- Class 1A NICs for 2025/26 are charged at 15% of the total cash equivalent of reportable benefits, due by 22 July 2026 for electronic payment.

- Gathering company car, medical insurance and loan data is often the most time-consuming part of P11D preparation.

- Common P11D errors include omitted benefits, incorrect valuations and unreconciled payroll data.

- From April 2027, most benefits in kind must be reported through payroll, with loans and accommodation remaining on the P11D.

- 2025/26 is the final full tax year before mandatory payrolling of most benefits begins in April 2027.

What does P11D Filing involve?

Employers must file a P11D for each employee or director who received taxable benefits or expenses during the tax year that were not processed through payroll.

A P11D(b) must also be submitted to declare the total Class 1A NICs owed on those benefits.

Key dates for 2025/26

| Obligation | Deadline |

|---|---|

| P11D and P11D(b) submission to HMRC | 6 July 2026 |

| Copy of P11D information to each affected employee | 6 July 2026 |

| Class 1A NICs, electronic payment | 22 July 2026 |

| Class 1A NICs, cheque | 19 July 2026 |

The Class 1A NICs rate for 2025/26 is 15% of the total cash equivalent of all reportable benefits. Any P11D(b) prepared without this rate will carry an incorrect figure.

Reportable benefits can include company cars and fuel provided for private use, private medical insurance, beneficial loans, living accommodation and other employer-provided benefits with a taxable value. Each benefit type has its own cash equivalent calculation under HMRC rules.

That means preparation involves more than compiling records. It requires applying the correct valuation method to each benefit before the return is filed.

A return that gets this right depends entirely on what the underlying records look like and that is usually where delays occur.

Common Challenges in P11D Preparation

Most P11D errors are not caused by misunderstanding the rules. They come from the records themselves: where they sit, how complete they are and whether they reflect changes made during the year.

Benefit records come from multiple sources

Company car records are usually held by a lease provider or fleet management system, private medical insurance records by HR, and beneficial loan information by the finance team. Payroll data rarely contains a complete record of non-payrolled benefits.

A business providing taxable benefits may need information from multiple teams before any figures can be confirmed.

Where records have not been maintained consistently during the year, data collection often takes longer than the preparation work itself.

Employee benefit changes add reporting complexity

Mid-year benefit changes require additional calculations. An employee who changed company vehicles during the tax year needs separate benefit calculations for each vehicle based on the correct availability period.

The same applies where employees leave during the year, opt in or out of fuel benefits, or have changes to their private medical insurance cover. Each change affects the final reportable value.

Benefit valuations follow specific HMRC rules

Incorrect valuations affect both the Class 1A NICs calculation and the employee’s tax position. Company car benefits depend on the vehicle’s list price, CO₂ emissions and availability dates.

Beneficial loan calculations require accurate loan balances, transactions during the year and the HMRC official rate of interest of 3.75% for 2025/26. Private medical insurance must be reported using the actual employer cost of the policy.

These calculations must be supported by source records rather than estimates. Many reporting issues arise because benefit information is held across different systems and teams.

Many of these issues arise from how benefit records are maintained throughout the year. Outsourcing changes how that information is reviewed and prepared for filing.

How can Outsourcing support P11D Filing?

Outsourcing P11D filing means a provider handles the preparation work while the employer keeps the underlying compliance responsibility. The provider prepares the P11D for each employee and the P11D(b) for the employer. Some providers submit directly to HMRC once the figures are confirmed.

Setting up the data request

A provider specifies the information required for each benefit category, the format needed and the submission deadline.

This replaces separate requests across payroll, HR and finance with a single structured information request at the start of the process.

Checking and calculating

Once records are received, the provider checks each benefit against HMRC’s valuation rules, calculates the cash equivalent for company cars, loans and medical insurance and works out the Class 1A NICs figure for the P11D(b).

Producing and filing the forms

The provider prepares the P11D for each employee and the P11D(b) for the employer. Some providers submit directly to HMRC once the figures are confirmed; others return completed forms for the employer or accountant to file.

Handling mid-year changes

A car changed mid-year, a new medical insurance policy or a loan partly repaid all need flagging early. A provider using a full year of records can calculate the benefit accurately rather than relying on a single point in time.

Supporting accounting practices

For practices managing several employer clients, outsourcing means each client’s return goes through this same process without competing for the same internal hours in June and July.

Outsourcing affects the preparation process, the review stage and the consistency of reporting across tax years. It changes how accurate the figures are, how much time internal teams spend on it and how consistent the process looks from one year to the next.

Benefits of Outsourcing P11D Filing

Outsourcing P11D preparation gives employers access to a structured process for gathering benefit data, applying HMRC valuation rules and preparing returns.

The main advantages typically relate to accuracy, time savings and consistency across reporting periods.

More accurate valuations

Providers specialising in P11D preparation apply HMRC valuation rules regularly as part of their preparation process. This includes using the correct official rate for beneficial loans, applying the appropriate CO₂ percentage for company cars and verifying medical insurance values against policy records.

Errors in any of these calculations can affect both the Class 1A NICs liability and the employee’s reported benefit value.

Less pressure on internal teams

P11D preparation draws on payroll, HR and finance at the point in the year when those teams are also closing year-end accounts and preparing for Corporation Tax deadlines.

Moving this work to a provider removes that demand from internal teams during the weeks it matters most.

A consistent process every year

P11D preparation handled internally is often done by whoever has time that year, using whatever format the records happen to be in. A provider applies the same checks every year regardless of which staff member is involved on either side.

For practices managing several employer clients, this also means each return goes through the same review process before the 6 July deadline.

A consistent process reduces how often things go wrong. The next section looks at what those errors usually are and what they cost when they happen.

Common Reporting Errors and Filing Risks

The errors below are the ones that show up most often when P11D records are reviewed close to the deadline. Each one connects back to a gap in the data collection stage covered earlier, rather than a misunderstanding of how P11D works.

| Error type | Why it occurs |

|---|---|

| Omitted benefits | A benefit was provided during the year but not recorded at the time, so it does not appear in the records used for preparation |

| Incorrect company car valuations | Wrong list price, outdated CO2 figure or incorrect availability dates used in the calculation |

| Beneficial loan errors | Loan balance not updated for repayments or the official rate of interest applied does not match the rate for the period |

| Private medical insurance discrepancy | Policy cost changed during the year but the updated figure was not recorded |

| Payroll and benefit data mismatch | Payroll records and benefit-in-kind data have not been reconciled before submission |

| Missing nil return notification | Employer received a P11D(b) reminder, had nothing to report and did not notify HMRC |

Take the mid-year company car change covered earlier as an example. If the replacement vehicle’s details are not added to the records used for P11D preparation, the calculation applies the original vehicle’s figures for the period after it was returned.

The result is a cash equivalent that gets the benefit wrong for part of the year and this is difficult to spot without checking the vehicle availability dates against the actual change date.

Penalties for Late or Incorrect Filing

HMRC charges a penalty of £100 per 50 employees for each month or part month a P11D(b) remains unfiled after 6 July. This applies automatically and without a grace period.

Interest applies separately to Class 1A NICs paid after 22 July 2026.

These penalties are separate from the impact on employees. An overstated benefit can result in too much tax being collected through PAYE. An understated benefit may lead to HMRC issuing a revised tax code to recover the shortfall, reducing the employee’s take-home pay until the amount is repaid.

Avoiding these errors starts before preparation even begins, with the information an employer hands over at the outset.

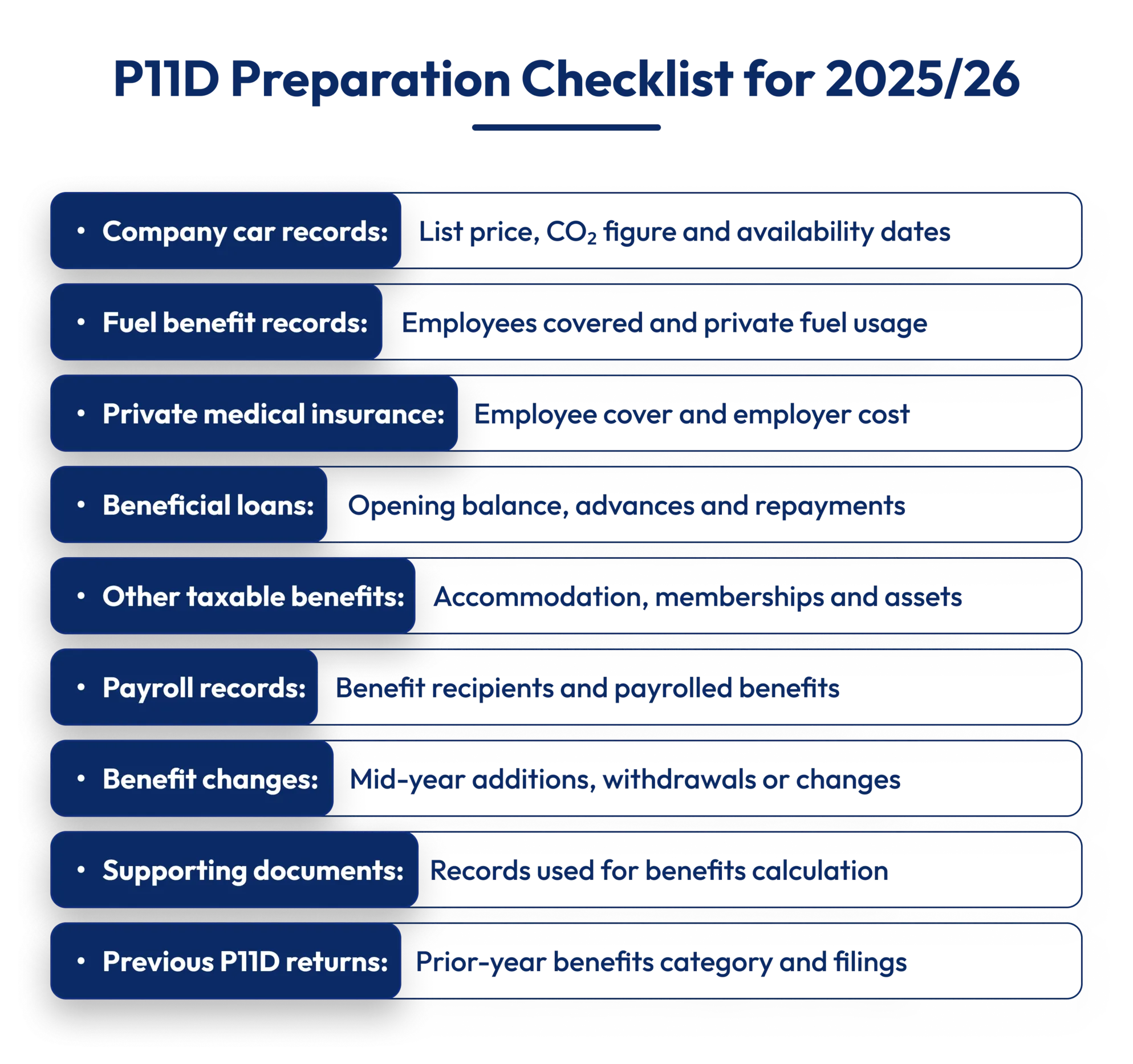

Information to prepare before Engaging a Provider

The accuracy of a P11D return depends on the quality of information supplied at the start. Preparing the following in advance reduces the queries that come back during preparation and the corrections needed after the first draft.

Where records are incomplete, identifying the gaps early gives more time to resolve them before preparation begins.

Once this information is ready, the choice of provider determines how much of the remaining work still sits with the employer or practice.

Key considerations when Choosing a Provider

Choosing a provider involves more than comparing costs or turnaround times. The right option depends on how the provider handles filing, reviews benefit data, protects employee information and manages reporting deadlines.

The factors below help assess whether a provider is suited to your reporting requirements.

Direct HMRC filing or preparation only

Some providers prepare P11D and P11D(b) forms for the employer or accountant to review and submit.

Others file directly with HMRC through PAYE Online or approved payroll software. For accounting firms managing multiple employer clients, knowing which arrangement applies and what authorisation direct filing requires, matters before any engagement starts.

Validation and review procedures

A provider should explain clearly what happens between receiving the data and producing the final return.

Do they reconcile payroll records against benefit data? Do they flag missing information before preparing valuations? Do they provide workings for review or deliver completed forms only?

These questions affect the accuracy of the return and how much correction work is needed after the first draft.

Turnaround and capacity

Turnaround matters most for accounting practices managing multiple client returns against the same 6 July deadline.

Confirm the expected timescale from data receipt to draft return, how amendments are handled and whether the provider has capacity during June and early July.

Data security

P11D preparation involves employee personal data including National Insurance numbers, benefit values, salary information and loan details.

Before transferring any information, confirm how the provider stores and transmits data, what security standards apply and how data is handled at the end of the engagement.

Experience with specific benefit types

A provider who regularly prepares returns involving taxable benefits applies the correct valuation rules without guidance.

A provider with limited experience of a particular benefit type may need additional input, which shifts work back to the employer or accountant.

Ask specifically about the benefit types in scope before proceeding. The provider selected for the current filing cycle may also support the transition to mandatory payrolling from April 2027.

Preparing for Future Reporting Changes

From April 2027, HMRC requires most employers to report benefits in kind in real time through payroll software, replacing the annual P11D submission for the majority of benefit types. The 2025/26 tax year is the last full traditional P11D cycle for most employers.

| Benefit Type | After April 2027 |

|---|---|

| Company cars, fuel benefits, private medical insurance and most other benefits in kind | Reported in real time through Full Payment Submission via payroll software |

| Employment-related loans | Remains on P11D process |

| Living accommodation | Remains on P11D process |

Employers providing beneficial loans or living accommodation keep P11D obligations after the transition. For all other benefit types, annual P11D reporting is replaced by real-time payrolling through each pay run.

A provider engaged for P11D preparation this year who already knows the employer’s benefit structure is better placed to support that transition. The benefit records reviewed for 2025/26 feed directly into the payrolling workflow from April 2027.

This year’s filing, then, is not an isolated task. It sets up how the move to real-time reporting goes for everyone involved.

Conclusion

P11D preparation means identifying reportable benefits, applying the correct valuation rules, reconciling records across multiple data sources and submitting accurate returns to HMRC by 6 July 2026. These are specific tasks with specific requirements and getting them wrong carries direct consequences for both employers and the employees whose tax codes are affected.

The 2025/26 cycle also matters beyond the immediate deadline. It is the last full year of traditional P11D filing for most benefit types before mandatory real-time payrolling begins in April 2027. Accurate records and a well-managed return this year support that transition.

Outbooks works with UK employers and accounting firms on P11D preparation and filing. For support ahead of the 6 July 2026 deadline, contact the team at +44 330 057 8597 or email us at info@outbooks.co.uk.

FAQs

Can a business outsource P11D preparation without outsourcing its full payroll?

Yes, P11D preparation can be outsourced independently. The provider uses benefit records and employee data supplied by the business and does not need access to the day-to-day payroll function.

What is the difference between voluntary payrolling and traditional P11D filing?

Voluntary payrolling taxes benefits through the payroll each month. Employers registered to payroll specific benefits before 2025/26 do not file individual P11Ds for those benefits, though a P11D(b) is still required for Class 1A NICs.

If a benefit was provided for only part of the tax year, does it still need to be reported?

Yes, the cash equivalent is pro-rated to reflect the period the benefit was available, but the obligation to report applies regardless of how long the benefit lasted.

Does outsourcing P11D filing transfer legal responsibility for errors to the provider?

No, the employer remains legally responsible for accuracy. Outsourcing transfers the preparation work, not the compliance obligation. Errors from incomplete information supplied to the provider remain the employer’s responsibility.

What should an accounting firm assess when selecting a P11D provider for multiple clients?

Capacity, process consistency and communication. The provider must handle volume across multiple employer clients at the same time and raise queries before the 6 July deadline, not after the draft has been reviewed.

Which benefits remain on the P11D process after April 2027?

Employment-related loans and living accommodation remain on the P11D process after April 2027. All other benefit types move to real-time reporting through payroll software.

What happens to an employee’s tax position if a benefit is reported incorrectly?

HMRC adjusts employees’ tax codes using P11D data. An overstated benefit means excess tax collected through PAYE. An understated benefit may lead to a revised code recovering the shortfall, reducing the employee’s take-home pay.

Can directors of owner-managed businesses have benefits reported on a P11D?

Yes, directors are treated as employees for P11D purposes. Taxable benefits provided to directors are reported in the same way as benefits for any other member of staff.

What is the nil return notification and when does it apply?

If an employer receives a P11D(b) reminder but has no taxable benefits to report, they must notify HMRC that no return is due. Not doing so leaves an expected filing on record and generates automatic penalty charges.

Is outsourcing P11D filing cost-effective for small businesses?

Yes, particularly where employees receive multiple taxable benefits or internal teams have limited capacity. Outsourcing can reduce preparation time, improve accuracy and lower the risk of corrections, penalties and additional administrative work after submission.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.